Popularity of buy now, pay later plans is on the rise this holiday season, according to survey

Canva

Popularity of buy now, pay later plans is on the rise this holiday season, according to survey

A couple lie on the carpet in their sitting room and shop online from a laptop; a Christmas tree is lit in the background

It’s tempting to try to extrapolate the health of the economy from a few days of shopping after Thanksgiving Day—just ask the business journalists filing all those Black Friday, Cyber Monday, and Giving Tuesday articles in between bites of turkey sandwiches.

While we really won’t know how festive or miserly shoppers were for a few more weeks, we can now be at least certain of one thing: Based on an Experian survey and preliminary data from retail monitors, it’s already the biggest year ever for buy now, pay later (BNPL) plans. These plans allow eligible consumers to repay purchases with a short payment plan (four equal payments over several weeks is typical), providing some flexibility during a demanding shopping season.

To conduct its survey, Experian asked 1,012 consumers about BNPL plans on November 28, 2023. The sample was collected using a third-party company and was not from Experian’s consumer credit database.

![]()

Experian

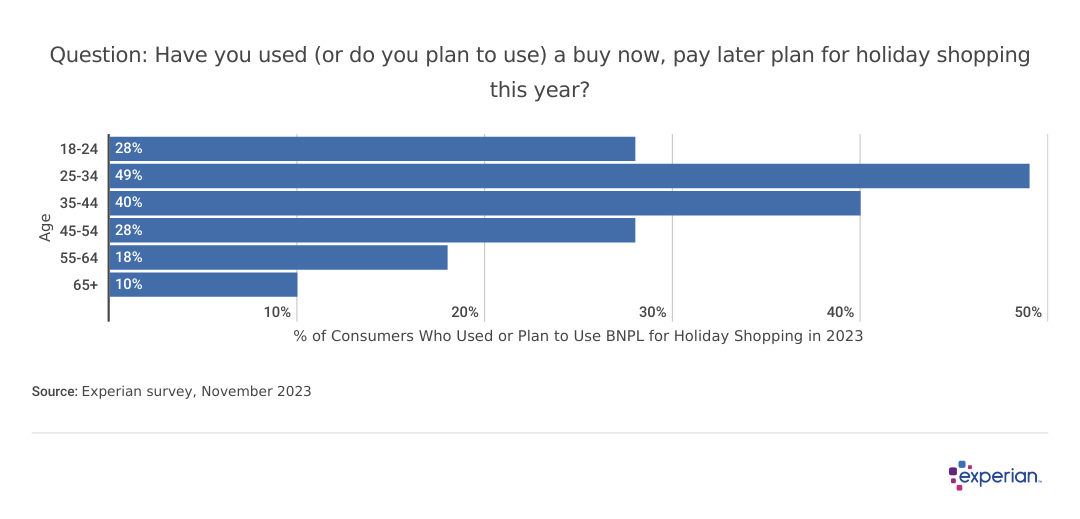

Buy now, pay later is part of 1 in 5 consumers’ holiday plans

Chart for: Age groups – Have you used (or do you plan to use) a buy now, pay later plan for holiday shopping this year?

Buy now, pay later plans won’t completely replace credit card spending anytime soon. About half of U.S. consumers, some 137 million people, made at least one credit card purchase on every Black Friday since 2020, according to Pymnts Intelligence. But buy now, pay later plans are playing an increasingly larger role in holiday spending.

On Cyber Monday alone, consumers spent nearly a billion dollars using buy now, pay later plans, a 42.5% increase over 2022, according to Adobe Analytics, which tracks consumer retail spending.

This was consistent with what consumers told Experian regarding how they expect to pay for their holiday shopping: Overall, 20% plan to use buy now, pay later plans as at least part of their holiday spending strategy this season.

Buy now, pay later plans are gaining popularity among all segments of the population, including older consumers and those with higher incomes. Adoption rates are highest among younger consumers, however: Nearly half of consumers ages 25 to 34 say they plan to use buy now, pay later for at least some of their holiday purchases in 2023. Adoption rates decline steadily the older the shopper, with only 10% of those age 65 or older expecting to use buy now, pay later.

Experian

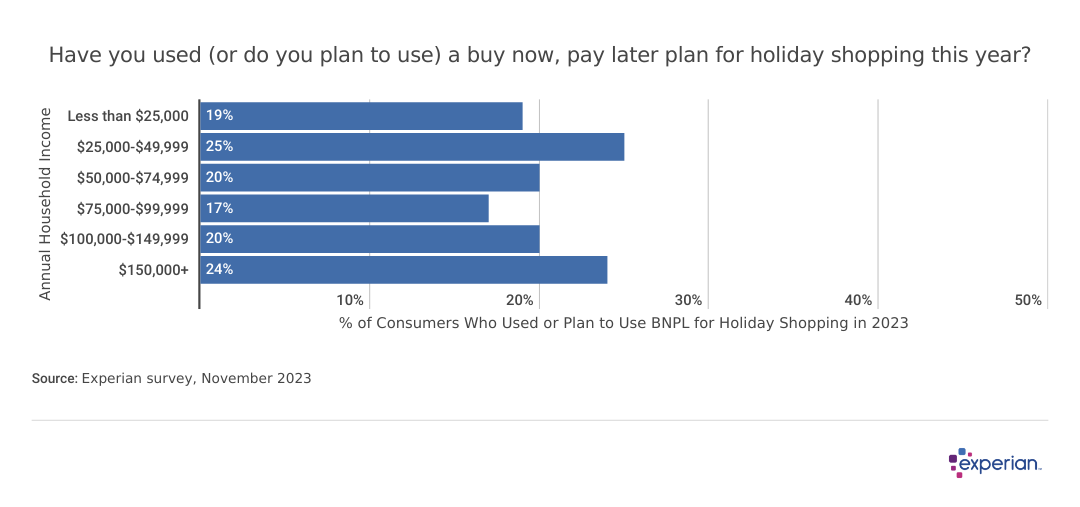

Household income not a factor for buy now, pay later usage

A bar chart: Question: Have you used (or do you plan to use) a buy now, pay later plan for holiday shopping this year?

Although buy now, pay later plans may appear to be a source of financing preferred among some lower-income consumers, Experian data indicates that income isn’t a factor in determining who uses the plans. Somewhat surprisingly, those with higher incomes are about as likely as those with lower incomes to use buy now, pay later plans.

One major incentive for consumers to use buy now, pay later may be interest-free payments. Consumers face interest rates averaging close to 23% APR on credit card balances, and may be reluctant to place additional holiday spending on cards—especially considering the average credit card balance was $6,365 in mid-2023, according to Experian data. Significant percentages of population segments—even millionaires—carry interest-accruing credit card debt.

Experian

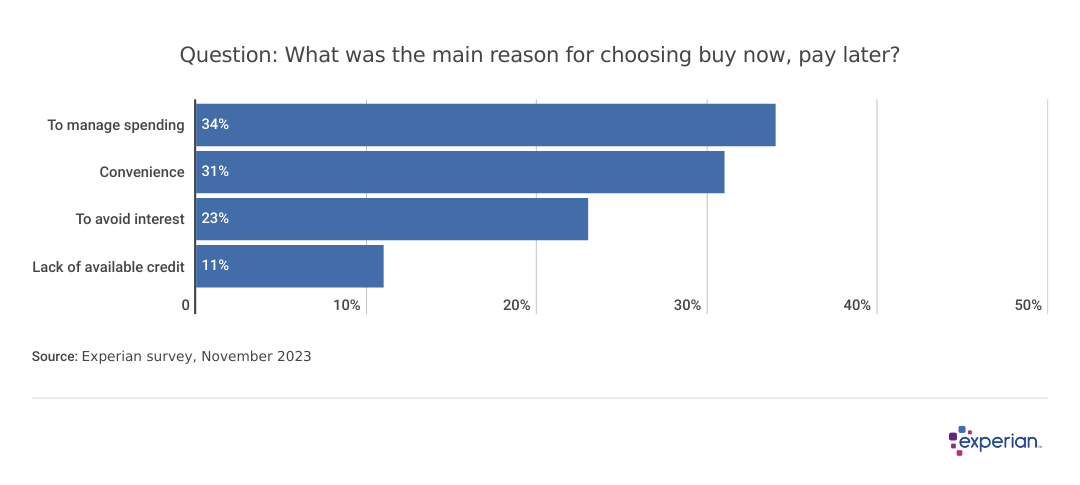

A convenient budgeting tool that avoids interest

Chart -What was the main reason for choosing buy now, pay later?

Among those who said they plan to use buy now, pay later to pay for at least some of their holiday spending, controlling their spending was identified as the most important reason—though not by much. While 34% of consumers cited managing spending as a reason to use buy now, pay later, 31% said that convenience—a quality usually attributable to paying with a credit card—was also a factor.

Nearly a quarter of consumers cited avoiding interest payments as a reason to use buy now, pay later. But perhaps the more interesting finding was how few consumers—only 11%—cited the buy now, pay later option as a result of having no other funding alternatives for financing their spending.

The bottom line

As buy now, pay later plans become ubiquitous as a payment option for both online and in-person shopping, some expect the plans to become even more interwoven into the commercial life of consumers, not only in December but also in the other 11 months of the year.

While BNPL accounts are typically not reported to the three major consumer credit bureaus (Experian, TransUnion and Equifax), that growing usage still has the potential to affect a consumer’s credit. Missing multiple BNPL payments could cause the account to be sent to collections, which could appear on credit reports and affect credit scores. And over-reliance on buy now, pay later could result in high monthly payment obligations that may cause users to miss their existing bill payments, such as auto loan and credit card payments.

With the popularity of buy now, pay later among consumers—especially younger ones—likely to continue, the payment method could have an effect on the way we spend and save around the holidays for the foreseeable future.

This story was produced by Experian and reviewed and distributed by Stacker Media.