"I'd probably just die": 26% of employed Americans don't know how they'd cover expenses if they couldn't work for 3 years

Iryna Imago // Shutterstock

“I’d probably just die”: 26% of employed Americans don’t know how they’d cover expenses if they couldn’t work for 3 years

An older woman with disability looking up insurance information online using a laptop.

For many American workers, the period from November to mid-January is open enrollment season, when they can sign up for or renew employer-sponsored health and disability insurance plans. Though fewer employers offer long-term disability insurance compared to health insurance, it’s a valuable benefit that helps replace part of your income if you’re ill or injured and can’t work.

However, according to the Policygenius Disability Preparedness Survey, less than one-third (31%) of working U.S. adults currently have any long-term disability insurance (LTDI) at all, while 51% of those without disability insurance don’t have it even though their workplace offers it.

At the same time, many working Americans are unprepared for an unforeseen illness or injury that makes it impossible for them to work. Twenty-six percent don’t know how they would cover living expenses if they couldn’t work for three years — a prospect that leaves some resigned: “I’d probably just die,” one worker told Policygenius.

Key findings:

- 26% of employed American adults don’t know how they would cover their living expenses if they couldn’t work for up to three years.

- 22% said they would either take on higher credit card debt or take out private loans to cover their expenses during an out-of-work period.

- Only 18% of employed U.S. adults are “very confident” that they could cover their expenses if they couldn’t work for up to three years.

- 26% of middle-income American workers would take on some sort of debt to cover their expenses if they couldn’t work for up to three years, and 45% are not confident they could cover their expenses during this time.

- 42% of middle-earning parents are not confident they’d be able to cover their expenses.

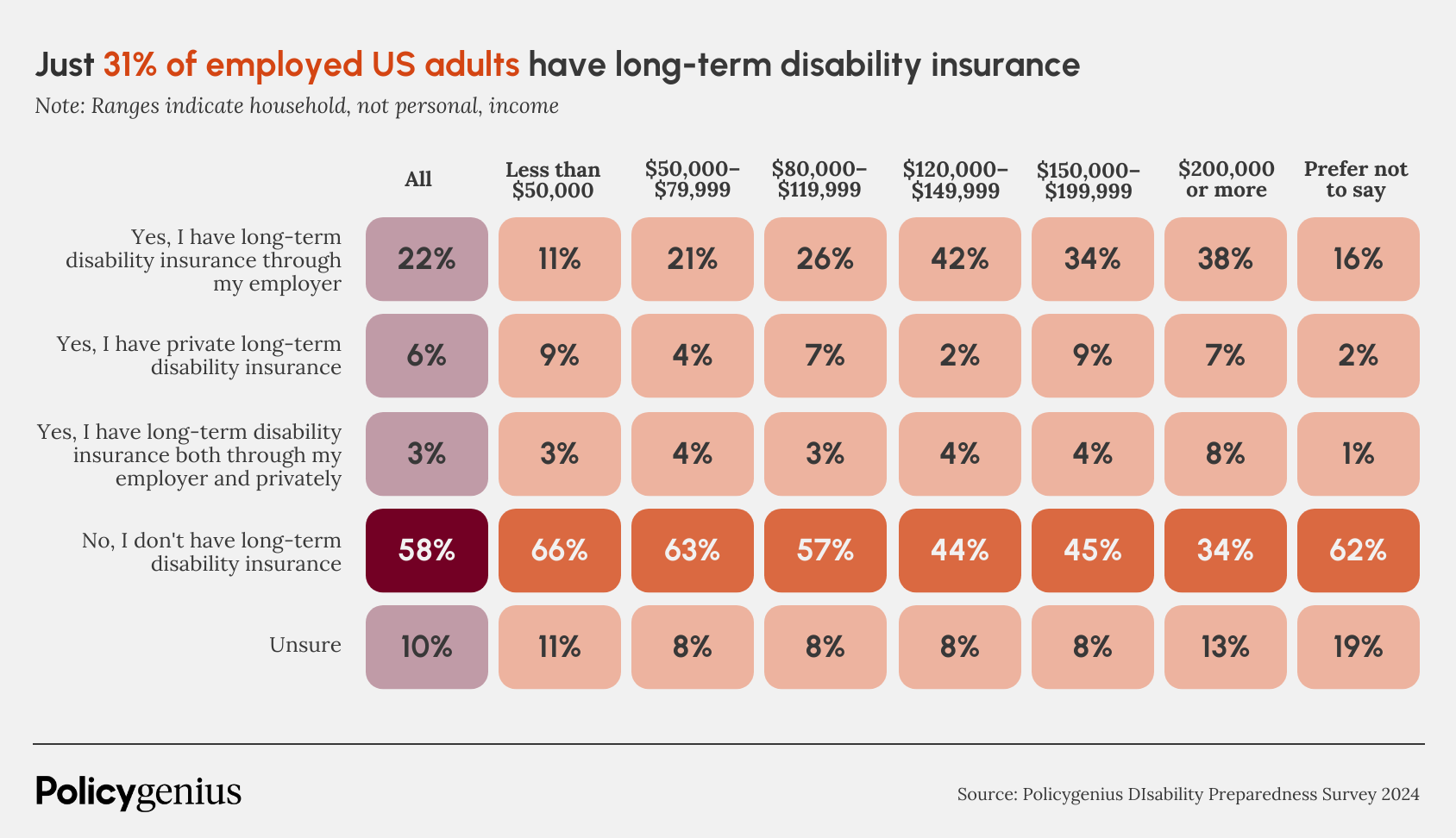

- Only 31% of employed U.S. adults have LTDI, either through their employer, a policy they bought on their own, or both.

- 58% don’t have LTDI at all, and 10% aren’t sure if they do or not.

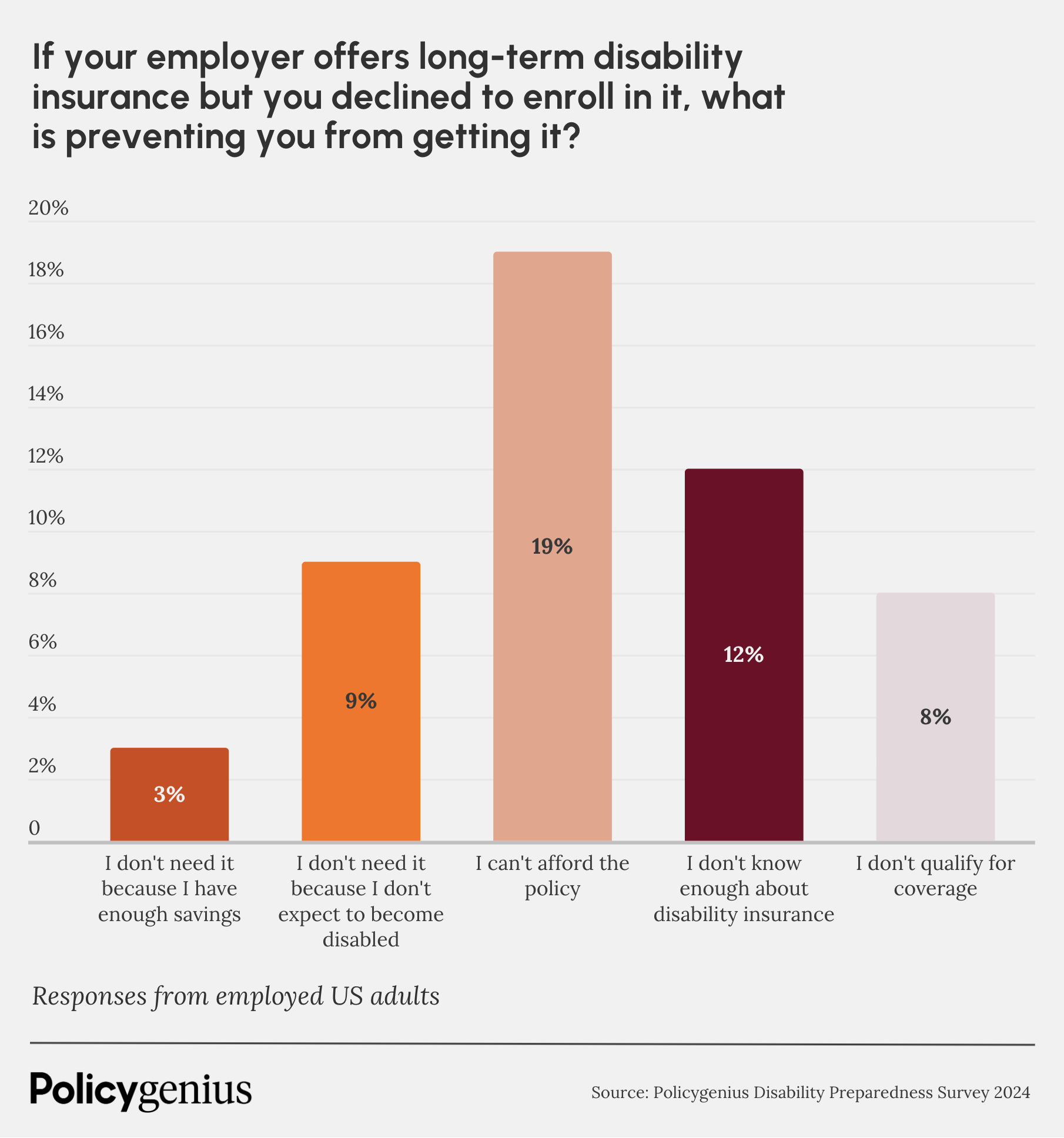

- Of those who don’t have LTDI, 49% say their employer doesn’t offer it, while 37% of those whose employers do offer coverage didn’t enroll in it because they can’t afford it.

What we mean by middle income

For the purposes of this survey, middle income refers specifically to those workers with annual household incomes of $80,000 to $149,999. This spans most of the range that the Pew Research Center defines as middle-income or middle-class: households earning between about $62,000 to $187,000 annually in 2022.

Many Employed Americans Don’t Have a Safety Net if They Are Unable to Work

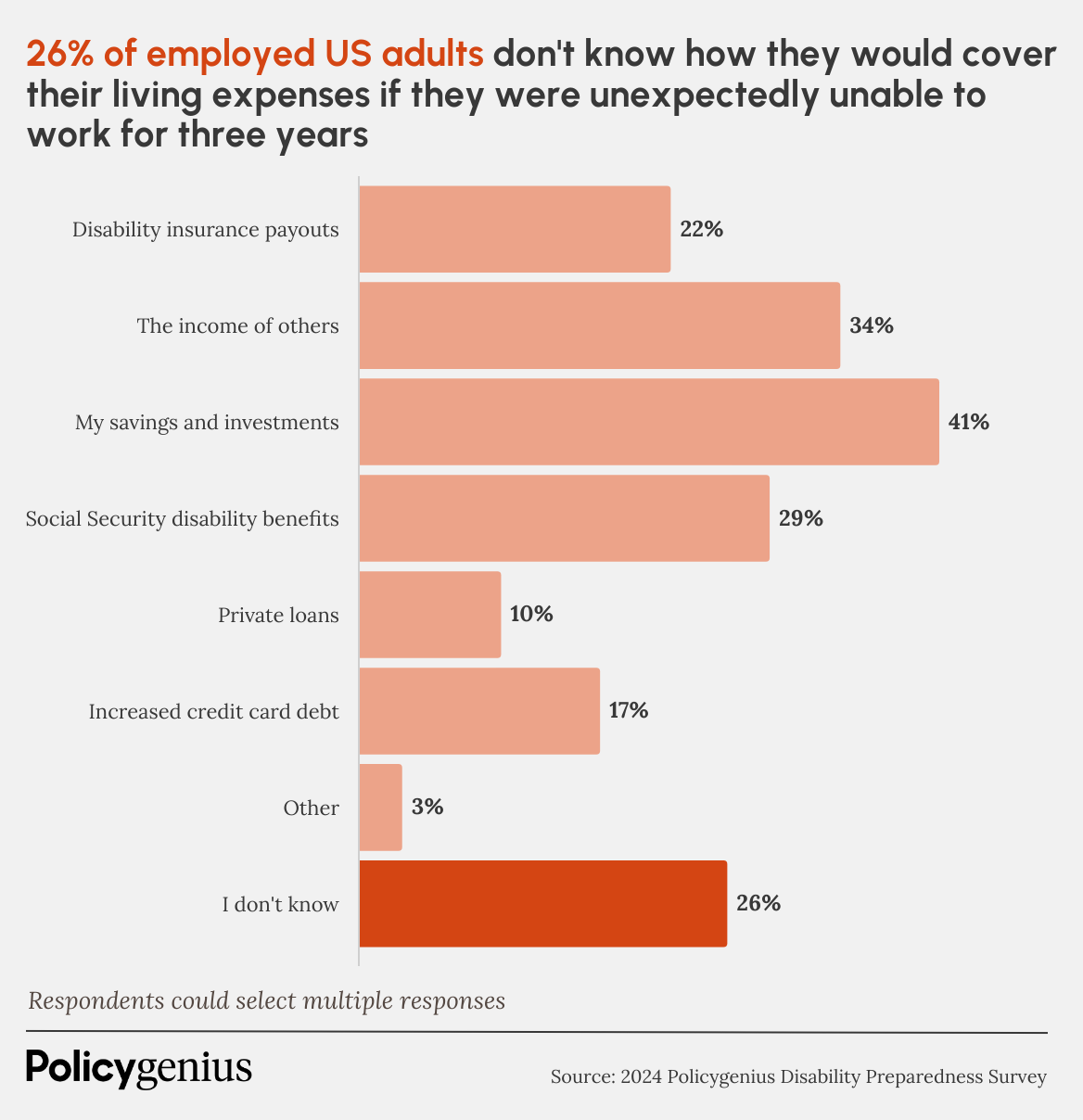

Roughly one in four employed Americans (26%) don’t know how they would cover expenses if they couldn’t work for up to three years. (The average length of a disability insurance claim is 34.6 months, according to the Council for Disability Income Awareness.) More than one-fifth (22%) would take on higher credit card debt or private loans. More specifically, 17% would increase their credit card debt, and 10% would open private loans if they were unable to work for three years.

On the other hand, 41% of employed Americans say they would live on their savings and investments, while 34% would live on the income of a spouse, partner, or another family member. Only 22% would rely on private disability insurance.

![]()

Policygenius

26% of Middle-Income American Workers Would Take on Debt if They Couldn’t Work

Survey results to the question “If you became unexpectedly injured or sick and could not work for up to 3 years, which, if any, of the following would you use to cover living expenses?”.

Middle-income Americans are the most likely group of earners to take on debt if they can’t work. More than a quarter (26%) said they would take out private loans or increased credit card debt if they couldn’t work—greater than those with either higher or lower incomes.

This includes 25% of those with household incomes of $80,000 to $119,999 and 29% of those with household incomes of $120,000 to $149,999.

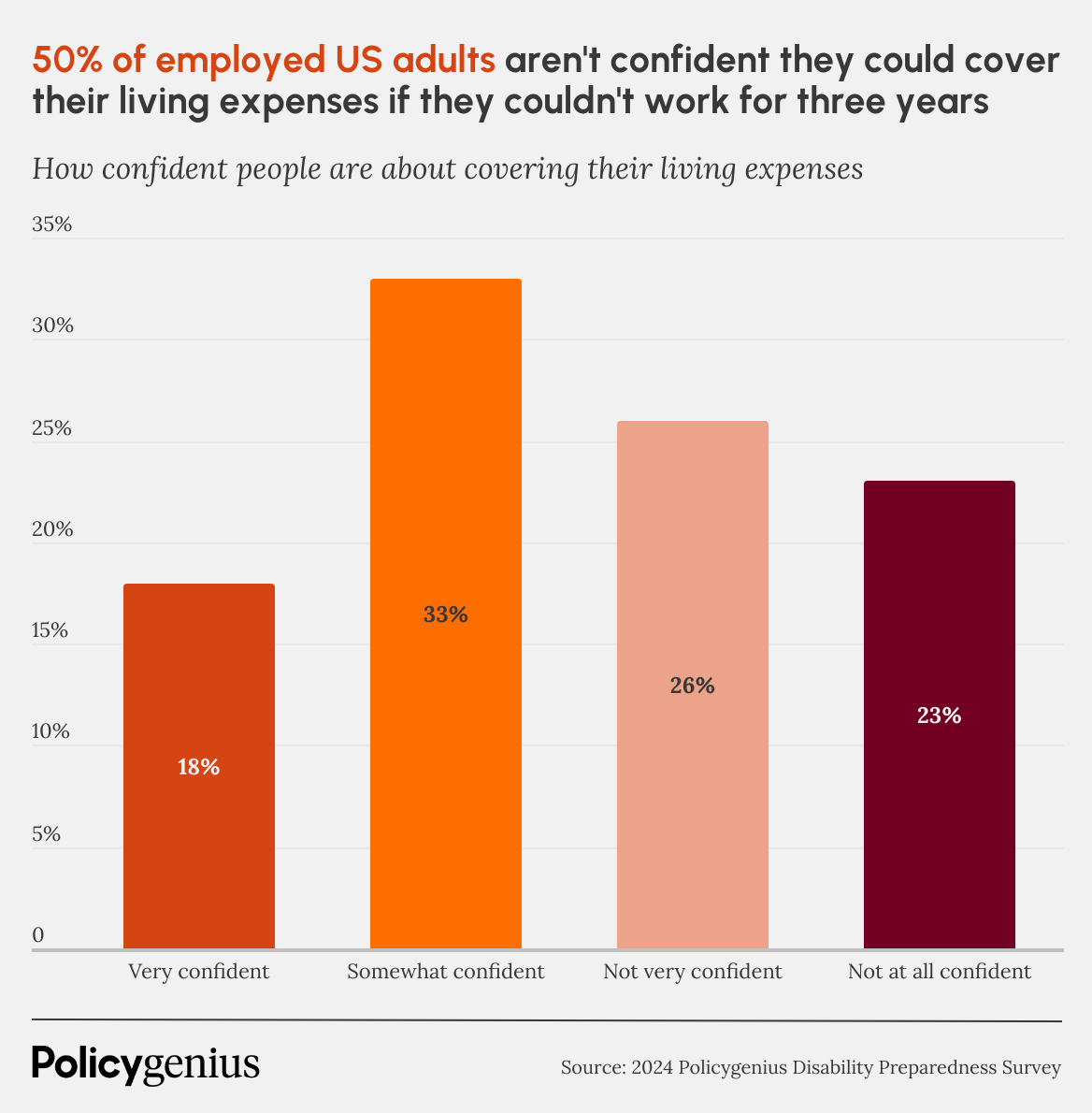

Half of Working Americans Aren’t Confident They Could Cover Their Expenses if They Couldn’t Work for 3 Years

Twenty-three percent of employed U.S. adults are “not at all confident” that they or their families could cover their living expenses if they were unable to work for this length of time, while an additional 26% are “not very confident.”

Meanwhile, only 18% are “very confident” that they could cover their living expenses while out of work for three years.

Policygenius

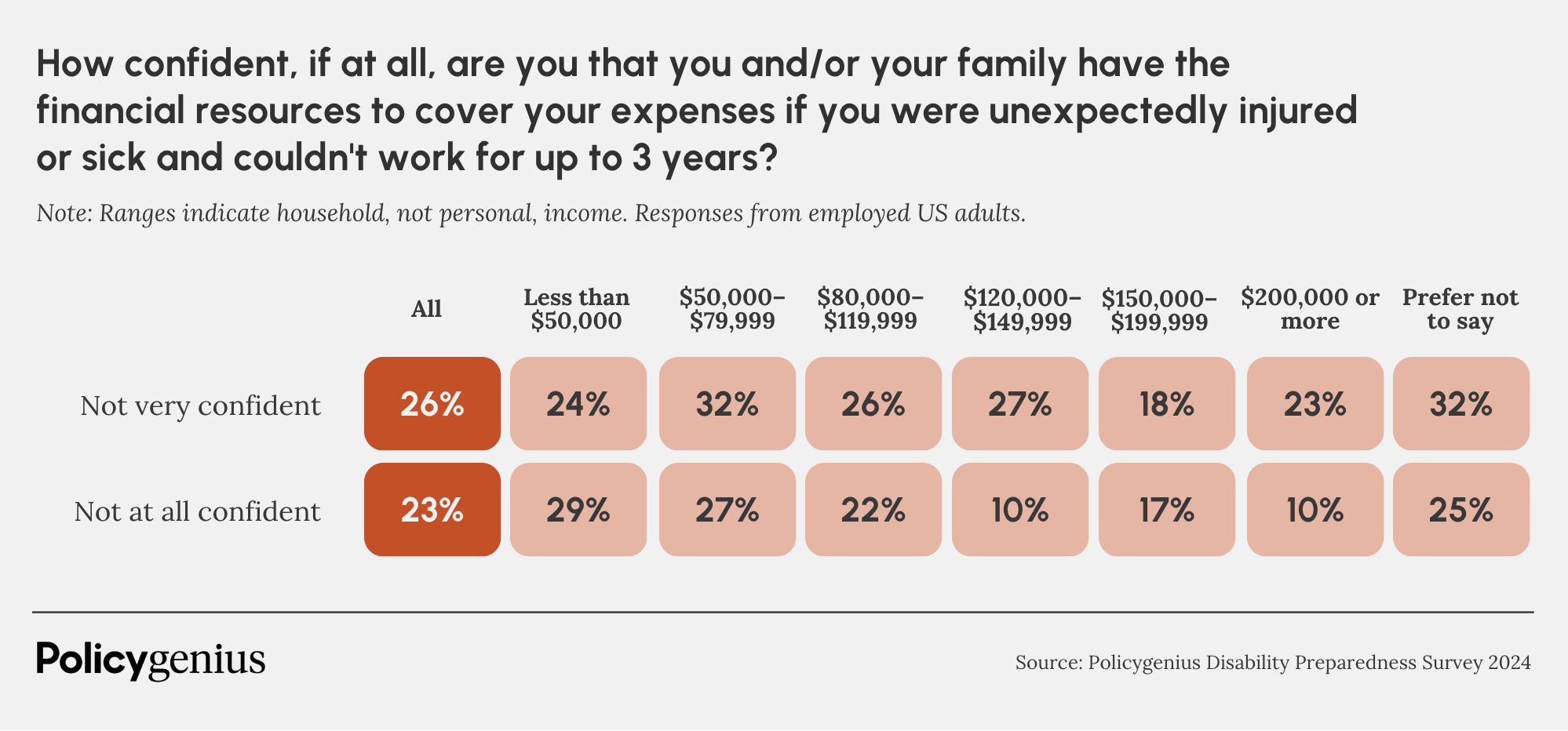

Confidence in Financial Resources Is Shaky for Both Low and Middle-Income Earners

Survey results to the question “How confident, if at all, are you that you and/or your family have the financial resources to cover your expenses if you were unexpectedly injured or sick and couldn’t work for up to 3 years?”.

The average yearly household spending in 2022 was $72,967, according to the most recent Consumer Expenditure Survey from the Bureau of Labor Statistics. Given this figure and the years of inflation since then, it’s not very surprising that only 14% of working Americans earning less than $50,000 a year are “very confident” they could cover their expenses during a long period of unemployment.

Many U.S. adults who are a part of middle-earning households aren’t confident either. In all, 45% of employed Americans with a household income of between $80,000 and $149,999 are either “not at all confident” or “not very confident” about covering their expenses if they couldn’t work.

This includes 47% of employed Americans with household incomes between $80,000 and $119,999 and 38% of employed Americans earning between $120,000 and $149,999, as well as 42% of parents in middle-earning households.

Policygenius

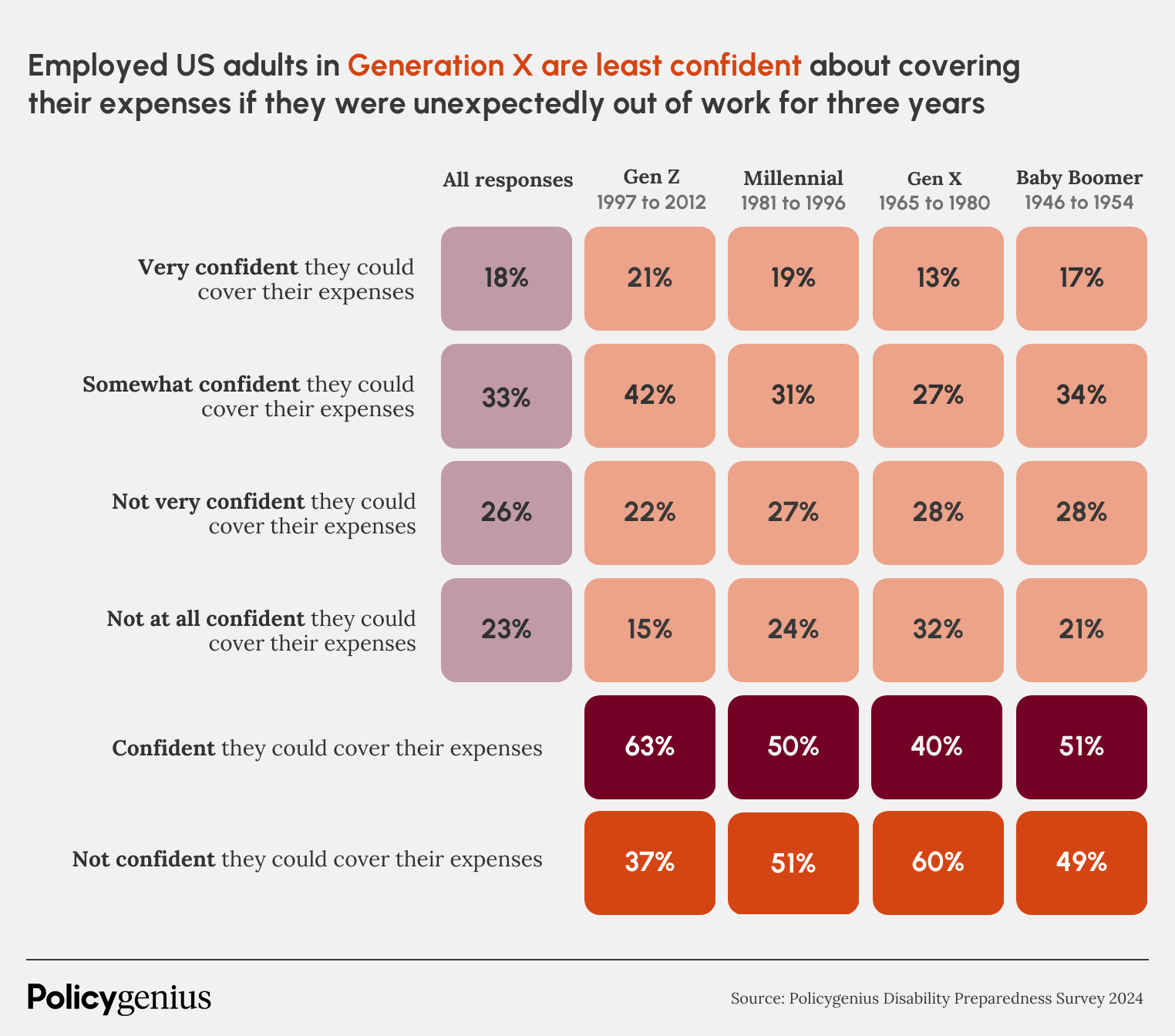

Generation X is the Least Confident About Covering Their Expenses, Though All Generations Are Similarly Pessimistic About It

Survey results to the question “How confident, if at all, are you that you and/or your family have the financial resources to cover your expenses if you were unexpectedly injured or sick and couldn’t work for up to 3 years?”

Generation X (workers who were born from 1965 to 1980) is the least confident of the generation groups Policygenius polled about covering their expenses. Sixty percent of Xers aren’t confident they could cover their expenses if they were out of work for three years, compared to about half of baby boomers and millennials and 37% of Generation Z.

Policygenius

Less Than a Third of American Workers Have LTDI, Even Though It Can Replace Lost Income for Years

Survey results to the question “How confident, if at all, are you that you and/or your family have the financial resources to cover your expenses if you were unexpectedly injured or sick and couldn’t work for up to 3 years?”.

If an injury or illness makes it impossible for you to work, LTDI may replace your income for years, usually until you’re 65 to 67 years old; that’s potentially millions of dollars in lost wages depending on your age and income.

American workers who have disability insurance tend to be more confident about covering their wages if they were out of work. Twenty-five percent of those with LTDI are “very confident” about covering their expenses, and another 37% are somewhat confident (62% combined, compared to 45% for those who don’t have LTDI).

However, only 31% of employed Americans have an LTDI policy, including just 39% of U.S. workers who make between $80,000 and $149,999 a year, and 54% of those earning $200,000 or more—those whose potential lifetime earnings are highest and who therefore stand to benefit most from having coverage.

Policygenius

Among Uninsured American Workers, 51% Don’t Have LTDI Even Though Their Employer Offers It

Survey results to the question “Do you have a long-term disability insurance policy?”.

Of uninsured American workers whose employers do offer LTDI, 37% didn’t enroll in a plan because they didn’t think they could afford it, including 32% of those with incomes of $80,000 or more a year. The same is true for 40% of parents and 29% of 18- to 34-year-olds—another group with high future earnings that benefits from having coverage.

Employer-provided disability insurance is often less than the cost of a private policy, which is usually somewhere from 1% to 3% of the insured person’s annual income.

Policygenius

What if your employer doesn’t offer long-term disability insurance?

Summary box: What can you do if you want disability insurance but your work doesn’t offer it and you don’t think you can afford it?

Private disability insurance usually costs more, but “it’s always better to have some disability insurance coverage than none,” says Patrick Hanzel, certified financial planner and Advanced Planning Manager at Policygenius. “But it’s also important to find an option that fits into your budget for as long as you need it.”

You don’t want to pay more than you can afford for a policy and risk it lapsing. Most disability insurance policies allow you to customize your coverage to maximize the features you need and remove the ones you don’t, which can help bring down the overall cost of your policy.

Methodology

Policygenius commissioned YouGov Surveys to poll a nationally representative sample of 2,505 adults aged 18 and older, including 1,416 workers. The survey was carried out online from Aug. 22 to Aug. 26, 2024. Figures have been weighted and are representative of all US adults aged 18+. The average margin of error for responses is +/- 2%. Percentages were rounded to the nearest whole number, so some totals may not add up to 100.

This story was produced by Policygenius and reviewed and distributed by Stacker Media.