What is an ICHRA? A guide to individual coverage HRAs

Valeri Luzina // Shutterstock

What is an ICHRA? A guide to individual coverage HRAs

A stethoscope on top of healthcare insurance costs and reimbursement documents.

ICHRA stands for Individual Coverage Health Reimbursement Arrangement, a type of health benefits plan that allows employers to reimburse employees for some or all of the premiums they pay for individual health insurance policies.

Key Points

- ICHRAs offer greater flexibility for employers and employees, allowing for personalized plan choices and contribution amounts.

- Employers can manage health care costs effectively by setting fixed reimbursement limits.

- ICHRAs provide tax-free reimbursements for both employers and employees.

- ICHRAs can enhance employee satisfaction by offering more choice and control over health care benefits.

Attracting and retaining top talent is vital to any business’s success, Thatch notes. But with rising healthcare costs, offering an extensive benefits package can feel like a financial burden. This is where ICHRAs come in.

An ICHRA is an employee benefits plan that gives employers a flexible way to provide tax-deductible reimbursements to employees for their individual health insurance premiums. This allows employees to choose a plan that best suits their needs and budget while offering employers greater control over health care costs and administrative burdens.

ICHRAs create opportunities for businesses of all sizes to better meet their employees’ needs. Small businesses are lining up to adopt ICHRAs, with recent data from the Health Reimbursement Arrangements Council indicating that small businesses represent a staggering 84% of the newest ICHRA adopters.

ICHRAs can also lead to significant cost savings for employers and employees, with a recent NPR story revealing that one small college saved $1.4 million in health care costs by switching to an ICHRA while their employees cut their premiums by an average of $1,200 each.

In the following sections, Thatch clarifies what an ICHRA is and isn’t, examines the benefits of ICHRAs for both employers and employees, and provides a step-by-step guide to help navigate implementing an ICHRA plan for businesses.

What Is An ICHRA?

ICHRAs allow employers to set aside a specific amount of money for each eligible employee. This money goes toward reimbursing the employee for a portion or all of their individual health insurance premiums. Employees have the freedom to choose a plan from the individual marketplace that best suits their needs, budget, and coverage preferences.

Compared to traditional plans, an ICHRA generally offers more personalization and flexibility. Choosing between the two can be a significant decision for employers, potentially impacting employee satisfaction and the bottom line.

Here are some key differences between ICHRAs and traditional health insurance:

- Flexibility: ICHRAs offer significantly more flexibility for both employers and employees. Employers can set contribution levels and eligibility criteria, while employees can choose individual health insurance plans that best suit their needs. In contrast, traditional plans typically offer a limited number of preselected plans for all employees, restricting their ability to choose coverage that aligns with their individual needs.

- Cost control: While both plans can help manage healthcare costs, ICHRAs provide employers with more control by allowing them to set fixed contribution amounts. Traditional group plans, on the other hand, can be unpredictable due to potential rate hikes, new fees, or changes in cost-sharing.

- Administration: Compared to traditional group plans, ICHRAs often involve less administrative burden for employers. There’s less paperwork involved as employees manage their own plans and claims. However, employers still have some responsibility for record-keeping and compliance with ICHRA regulations.

Ultimately, the decision between ICHRA and a traditional group health plan depends on an employer’s specific goals, budget, and employee demographics.

![]()

Thatch

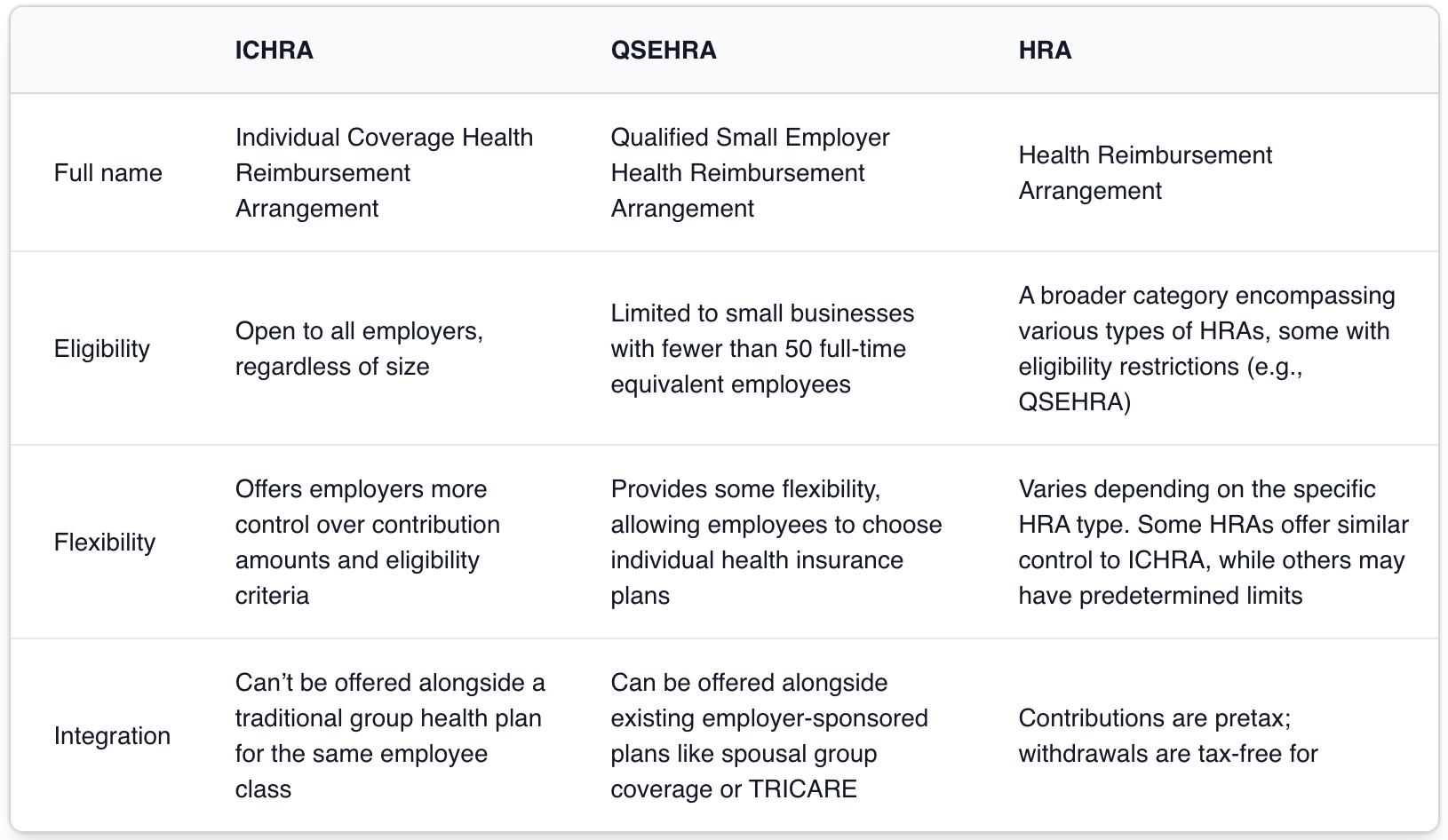

ICHRA vs. HRA vs. QSEHRA

Table showing differences between ICHRA and traditional health plans in categories of flexibility, control and cost.

Understanding the differences between ICHRA, QSEHRA, and HRA can be critical for businesses looking to offer their employees effective health benefits. While they share the common goal of reimbursing employees for health-related expenses, each plan has distinct characteristics.

By understanding these distinctions, employers can choose the health benefit plan that best aligns with their company’s size, budget, and employee needs.

Thatch

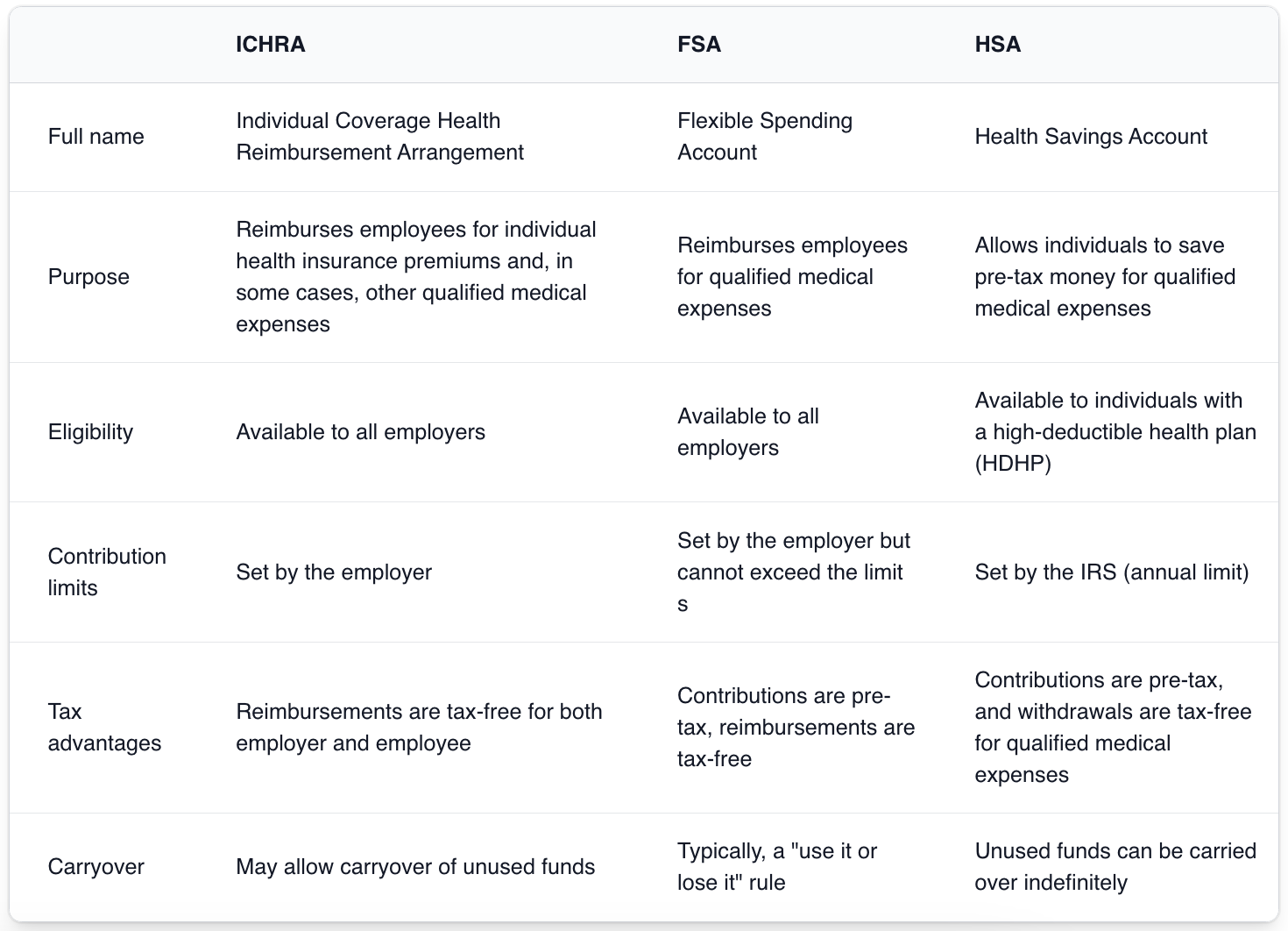

ICHRA vs. FSA vs. HSA

Table showing differences between ICIRA, QSEHRA, and HRA.

With acronyms like ICHRA, FSA, and HSA interspersed throughout insurance literature, navigating the world of health benefits can be confusing. These plans offer various ways to manage health care costs, but cater to different needs. To help understand their key differences, here is a handy chart that breaks down the important details about each plan.

As the chart shows, ICHRA, FSA, and HSA offer distinct advantages for managing health care costs. ICHRA offers employers greater flexibility in controlling contributions for individual health insurance premiums. FSAs are ideal for individuals with predictable medical expenses, while HSAs provide a long-term savings option for qualified medical expenses.

Thatch

Advantages and Benefits of ICHRAs

Table showing differences between ICHRA, FSA, HSA.

ICHRAs offer numerous benefits for both employers and employees. By empowering employees to choose their health insurance plans, ICHRAs can enhance employee satisfaction, improve retention rates, and contribute to a more positive work environment.

Through ICHRAs, employers can enjoy greater control over healthcare costs, tax advantages, and the potential to attract and retain top talent. With the flexibility to customize plans and the potential for cost savings, ICHRAs can be a valuable tool for businesses seeking to offer competitive and effective health benefits.

Thatch

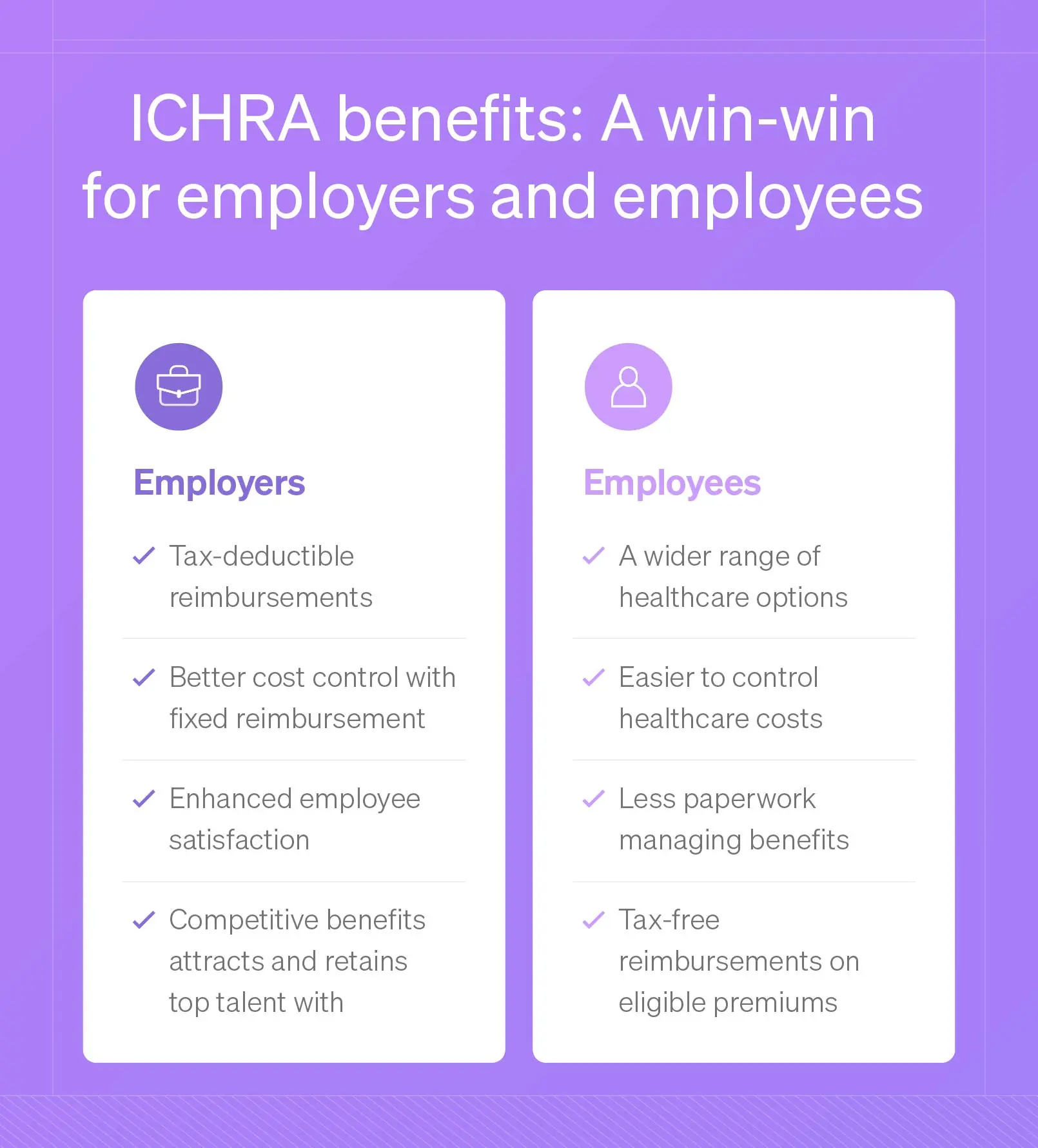

For Employers

List showing ICHRA benefits, why it is “a win-win for employers and employees”.

ICHRAs offer multiple advantages for employers seeking to effectively manage healthcare costs and provide attractive benefits to their employees.

- Cost management: ICHRAs give employers greater control over healthcare costs by setting fixed reimbursement amounts. This can help predict and manage expenses more effectively compared to traditional group health plans, which can be subject to fluctuating premiums and benefit changes.

- Tax advantages: ICHRAs offer significant tax advantages for employers. The reimbursements provided to employees are tax-deductible for the business, reducing its overall tax liability. This can lead to substantial cost savings for employers.

- Employee flexibility: By offering employees more choices in their health insurance plans, employers can demonstrate their commitment to employee well-being and potentially attract and retain top talent.

- Improved employee satisfaction and retention: Offering ICHRA as an employee benefit can enhance job satisfaction and help increase employee retention rates. Providing employees with greater choice and control over their healthcare allows employers to demonstrate their commitment to their well-being. This can lead to a more positive and engaged workforce.

For Employees

An ICHRA gives employees a degree of flexibility and control over their health care that is often not available with traditional group health plans.

- Expanded health care options: ICHRAs provide employees with a wider range of health insurance plans to choose from. This flexibility allows employees to find a plan that best suits their needs, budget, and coverage preferences.

- Tax advantages: Employees can benefit from tax advantages with ICHRA. The reimbursements they receive from their employer toward their individual health insurance premiums are generally tax-free, reducing their overall tax burden.

- Greater control over health care spending: ICHRAs empower employees to have more control over their healthcare spending. A plan that aligns with their specific needs can help employees avoid paying for unnecessary coverage and potentially save money.

- Portability: ICHRAs can offer greater portability compared to traditional group health plans. If an employee changes jobs or relocates, they may be able to continue using their existing individual health insurance plan under the ICHRA, providing continuity of coverage.

- Less paperwork: ICHRAs can often involve less paperwork for employees compared to traditional group health plans.

Thatch

How to Determine if It’s Right for Your Business

Graphic showing key factors to consider when choosing a plan.

When considering implementing an ICHRA plan, businesses should carefully evaluate several factors:

- Company size and structure: ICHRAs can be a valuable option for businesses of all sizes, but smaller businesses may find a QSEHRA more suitable due to its specific eligibility requirements.

- Employee demographics: Consider your employees’ age, health status, and income levels. ICHRA can be particularly beneficial for employees with unique healthcare needs or those seeking more flexibility in their plan options.

- Budgetary constraints: Assess your business’s financial resources and determine how much you can allocate towards employee health care benefits. ICHRAs can provide a cost-effective solution, but it’s important to set realistic reimbursement limits and manage costs effectively.

- Administrative capacity: Consider the administrative burden of managing an ICHRA plan. While ICHRA administration can be less complex than traditional group health plans, there are still administrative tasks involved, such as record-keeping and employee communications.

Legal and regulatory compliance

Understanding and adhering to ICHRA regulations is crucial for ensuring compliance and avoiding penalties. You’ll need to stay informed about federal and state-specific regulations that may apply to your business. Consulting with a benefits advisor or legal professional can help you navigate the complexities of ICHRA compliance.

Plan design

Whether you do it yourself or get assistance from an employee benefits broker, designing an effective ICHRA plan involves several key considerations.

- Reimbursement amounts: Determine the appropriate reimbursement amounts based on your budget and the desired level of employee support.

- Eligibility criteria: Establish clear eligibility criteria for employees participating in the ICHRA plan. Consider factors such as full-time employment status and length of service.

- Plan documents: Create comprehensive plan documents that outline the terms and conditions of the ICHRA plan, including contribution amounts, eligibility requirements, and reimbursement procedures.

Cost control

While ICHRAs can help manage healthcare costs, implementing strategies for cost control is essential.

- Set reimbursement limits: Establish reasonable reimbursement limits to control the total amount spent on employee healthcare.

- Employee education: Provide employees with information about cost-saving strategies, such as using generic medications, preventive care, and shopping for affordable plans.

- Plan monitoring: Regularly review your ICHRA plan to ensure it remains effective and aligns with your business objectives.

Keeping employees informed

Effective communication is vital for a successful ICHRA plan. Ensure that employees understand the plan’s benefits and limitations. Provide clear and concise information about eligibility requirements, reimbursement procedures, and available resources. Consider offering employee education sessions or online resources to help employees make informed decisions about their health insurance choices.

How to Get Started With An ICHRA

Implementing an ICHRA plan requires careful planning and execution. Generally, employers can implement an ICHRA at any time throughout the year. However, there may be specific timing considerations based on your company’s size and circumstances.

By following these steps and seeking guidance from qualified professionals, businesses can successfully integrate ICHRA into their benefits strategy.

1. ICHRA eligibility

Before proceeding with ICHRA implementation, verify your eligibility. While most employers can offer ICHRA, certain businesses may have specific requirements. For example, applicable large employers with over 50 full-time employees in the prior calendar year may need to offer affordable coverage to 95% of their employees and dependents.

2. ICHRA plan design

Designing your ICHRA plan involves several key considerations:

- Contribution amounts: Determine the amount you will contribute to employee reimbursements.

- Eligibility criteria: Establish who is eligible to participate in the ICHRA plan (e.g., full-time employees, part-time employees).

- Plan documents: Create comprehensive plan documents outlining the terms and conditions of the ICHRA plan.

3. ICHRA offer and acceptance

Once your ICHRA plan is comprehensively designed, you must offer it to your eligible employees. Provide clear communication about the plan’s benefits and how employees can enroll. Employees must then accept the ICHRA offer to participate.

4. Managing an ICHRA

Efficiently managing your company’s ICHRA plan entails several key elements, including:

- Inviting employees: Extend the ICHRA offer to eligible employees.

- Terminating employees: Establish procedures for terminating employee participation in the ICHRA plan.

- Reporting to the federal government: Ensure compliance with federal ICHRA reporting requirements.

ICHRA FAQ

Find answers to common inquiries here and get even more details in the ICHRA Glossary.

How do ICHRAs work?

Individual Coverage Health Reimbursement Arrangements allow employers to reimburse employees for some or all of their individual health insurance premiums through three basic steps:

- Employer setup: The employer establishes an ICHRA plan, sets a specific reimbursement amount, and sorts their employees into one of 11 ICHRA classes (such as full-time, part-time, hourly, etc.).

- Employee enrollment: Employees choose an individual health insurance plan from the marketplace.

- Reimbursement: The employer reimburses the employee for eligible premium costs, typically on a monthly basis.

The reimbursement is tax-free for both the employer and the employee, making it a financially advantageous benefit for both parties.

Who is ICHRA right for?

ICHRA can be a great fit for a variety of businesses! Smaller businesses and startups often find ICHRA’s flexibility and cost-control features appealing, offering employees more choices in their health care plans.

However, even larger companies, including those considered applicable large employers, can benefit from ICHRA’s ability to cater to diverse employee needs.

What are the drawbacks of an ICHRA plan?

ICHRA plans offer flexibility but also come with potential drawbacks. For employers, this means managing risks like over-reimbursement and navigating complex compliance. Employees may face a more complex decision-making process, potentially higher out-of-pocket costs, and increased administrative tasks. Additionally, employees not eligible for the premium tax credit may find ICHRAs more expensive than traditional group plans.

Taking the Next Step With ICHRA

Understanding ICHRAs is essential for businesses seeking to offer competitive and flexible health benefits. By empowering employees to choose their own individual health insurance plans, ICHRAs can enhance employee satisfaction, improve retention rates, and contribute to a more positive work environment.

For employers, ICHRAs can provide greater control over health care costs, tax advantages, and the potential to attract and retain top talent. With the flexibility to customize plans and the potential for cost savings, ICHRAs can be a valuable tool for businesses of all sizes.

This story was produced by Thatch and reviewed and distributed by Stacker.