Thousands of US communities forgo federal flood insurance

Steve Exum // Getty Images

Thousands of US communities forgo federal flood insurance

Debris and river mud being hauled off the French Broad River area after Hurricane Helene in Marshal, NC.

Catastrophic inland flooding in North Carolina, South Carolina, and Tennessee has made headlines across the country in recent months. Severe flooding in areas not typically associated with flood problems may have Americans wondering if they should buy federal flood insurance.

But National Flood Insurance Program (NFIP) coverage may not be available to everyone who wants it, Insurify reports.

Nationally, 2,279 communities don’t participate in the voluntary program that provides insurance against flood damage, according to the Federal Emergency Management Agency, or FEMA, and most homeowners policies won’t cover flood damage. Property owners in non-participating municipalities can’t buy federally backed flood insurance.

Often, non-participating communities are rural, and many have very small populations. Other communities may seem to have little to no risk of flooding, though some may be unaware of the true risk in their area.

Communities that don’t participate in the NFIP often “have horrible, inadequate flood maps,” Chad Berginnis, executive director of the Association of State Floodplain Managers, or ASFPM, told Insurify. “FEMA’s limited mapping budget goes to areas with risk, and your areas of higher risk are going to be bigger. In smaller communities, you’re going to have old, approximate flood data.”

A lack of good data and floodplain maps is a widespread problem for communities, Berginnis said.

“We have 3.5 million miles of streams, rivers, and coastlines in the country. We’ve mapped 1.2 million miles of them. We’ve only mapped a third of our floodplains.”

How the NFIP Works

FEMA manages the NFIP, which Congress created in 1968 with the National Flood Insurance Act. Homeowners, businesses, and renters can buy flood coverage through the NFIP Direct system or more than 50 insurance companies that work with FEMA.

In order to participate in the NFIP, communities must agree to regulate residential and commercial development in any floodplains that fall within the municipality’s boundaries. Communities can participate in the NFIP only if their adopted and enforced regulations meet or exceed NFIP criteria.

In participating communities, any property is eligible to buy NFIP coverage—even those outside a mapped floodplain. Currently, the NFIP underwrites approximately 5 million policies in over 22,600 communities across all 50 states and six U.S. territories.

Any area that receives rain can be at risk for flooding, and flooding is the most common natural disaster, causing the costliest damages, according to FEMA. Yet nearly one-third of all NFIP claims originate in areas outside high-risk flood zones.

Why Communities Don’t Participate

Berginnis, who spent a decade in Ohio’s state floodplain management office before joining ASFPM, said communities may forgo NFIP participation for multiple reasons.

Some have no identified floodplains in their boundaries. Others may have flood zones that are already off limits for development. Some may have considered the relative costs of initiating a floodplain management program—a prerequisite for NFIP participation—and chose not to participate in the program.

In such situations, town officials may decide participating isn’t worth the effort—especially if they don’t see demand from residents for flood insurance. A lack of penalties for non-participation may also be a factor, Berginnis said.

“Essentially, joining the [NFIP] is a very simple and straightforward proposition,” he said. “Typically, the community passes a resolution of intent to join the program. That’s something the [town] council could do, literally at their next meeting. Then, they adopt a set of regulations and standards that include designating someone to be the floodplain manager.”

Every state provides model fill-in-the-blank ordinances to make it easy for communities to create the regulations required to participate in the NFIP, he said. Once communities commit to participation, they must administer and enforce the regulations they adopted around development in floodplains.

“We’ve kind of made it easy in this country, in my opinion, for communities to participate, and remove all obstacles for them participating,” Berginnis said. “They just need the political will to do it.”

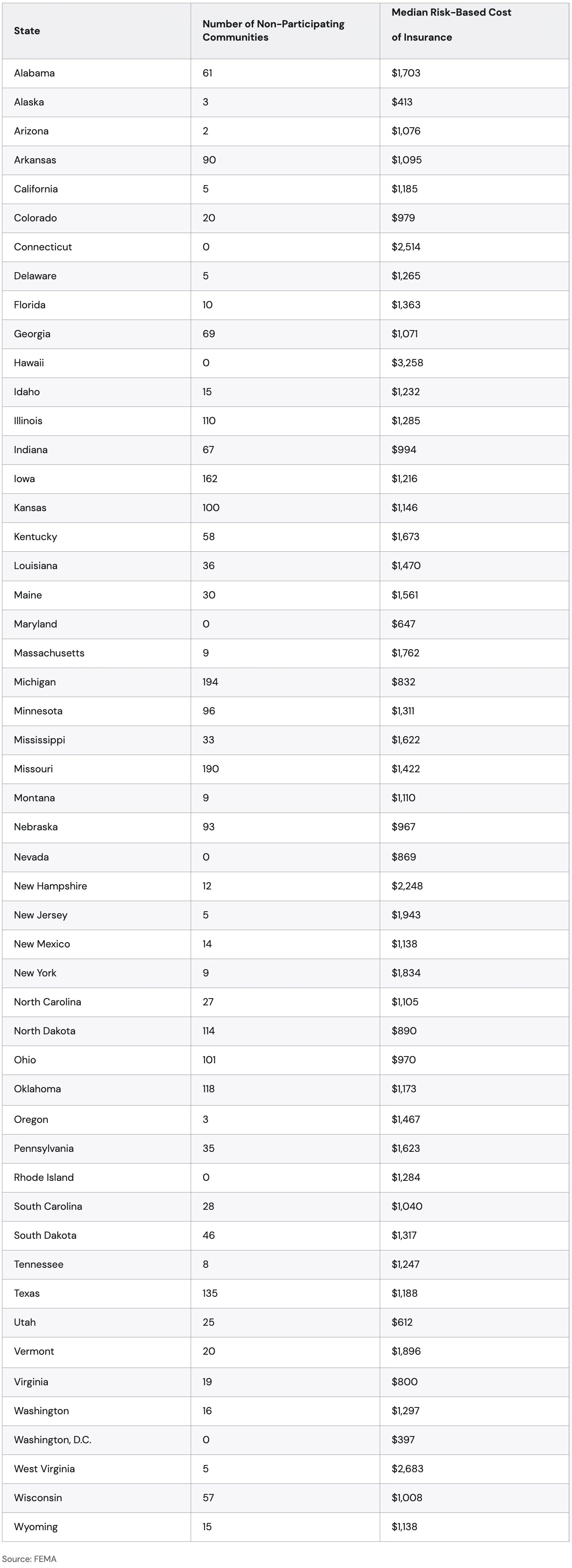

![]()

Insurify

Consequences of Non-Participation

Table showing number of non-participating communities and median cost of insurance in 50 states.

Residents of non-participating communities can’t buy federally backed flood insurance. They may also struggle to find private flood insurers willing to cover their properties, as some private insurers won’t sell flood coverage in areas that don’t take part in the NFIP.

Additionally, residents won’t be able to use federally backed mortgages, such as loans from the Department of Veterans Affairs, Federal Housing Administration, or Rural Housing Services, to buy or build a home in a Special Flood Hazard Area, or SFHA. And, if disaster strikes—as it did on Sept. 27 for many Western North Carolinians—non-participating communities won’t be able to secure financial assistance from the federal government to repair or rebuild structures in SFHAs.

The Tragic Example of North Carolina

Perhaps no state is a better example of the potential consequences of unprotected flood risk than North Carolina. Most of North Carolina’s 550 municipalities participate in the NFIP. But 27 don’t—including Mills River, which experienced damage in Hurricane Helene.

Helene ripped through the northwestern part of the state on Sept. 27, decimating communities in North Carolina’s largely rural Blue Ridge and Appalachian mountain ranges. The storm killed more than 225 people, and about half of those deaths were in North Carolina. As of October, authorities were still unsure how many people remained missing.

Flood damage to homes and businesses in affected communities is extensive. Since many affected communities are participants in the federal program, the NFIP could cover those losses, at least in part. But few property owners in those areas purchased NFIP policies before Helene.

For example, Asheville, with a population of more than 95,500 and 47,606 housing units, saw nearly 10 inches of rainfall that caused devastating flooding. But city residents and businesses had just 447 NFIP policies in force, offering total coverage of just under $152 million. Helene’s total cost could range as high as $250 billion, according to AccuWeather.

North Carolina’s Non-Participating Communities

At least one Tarheel community that saw damage from Helene doesn’t participate in the NFIP.

The town of Mills River in Henderson County lies south of the Asheville Regional Airport—and the Mills River. After Helene, the town’s Mills River Park became a distribution point for food, water, and supplies, and offered a mobile shower station, and mobile kitchen serving hot meals for storm victims.

The town was home to more than 7,300 people, according to the North Carolina League of Municipalities. Because the community doesn’t participate in the NFIP, most—if not all—homeowners and businesses in the town lack flood insurance and will have to shoulder the cost of rebuilding without federal funding.

Many of the North Carolina communities that don’t participate in the NFIP have very small populations of fewer than 1,000 residents. Like Mills River, they also tend to be rural. Many exist in close proximity to a number of waterways, from large rivers and lakes to creeks and streams. With inland waterways comes an elevated risk of inland flooding.

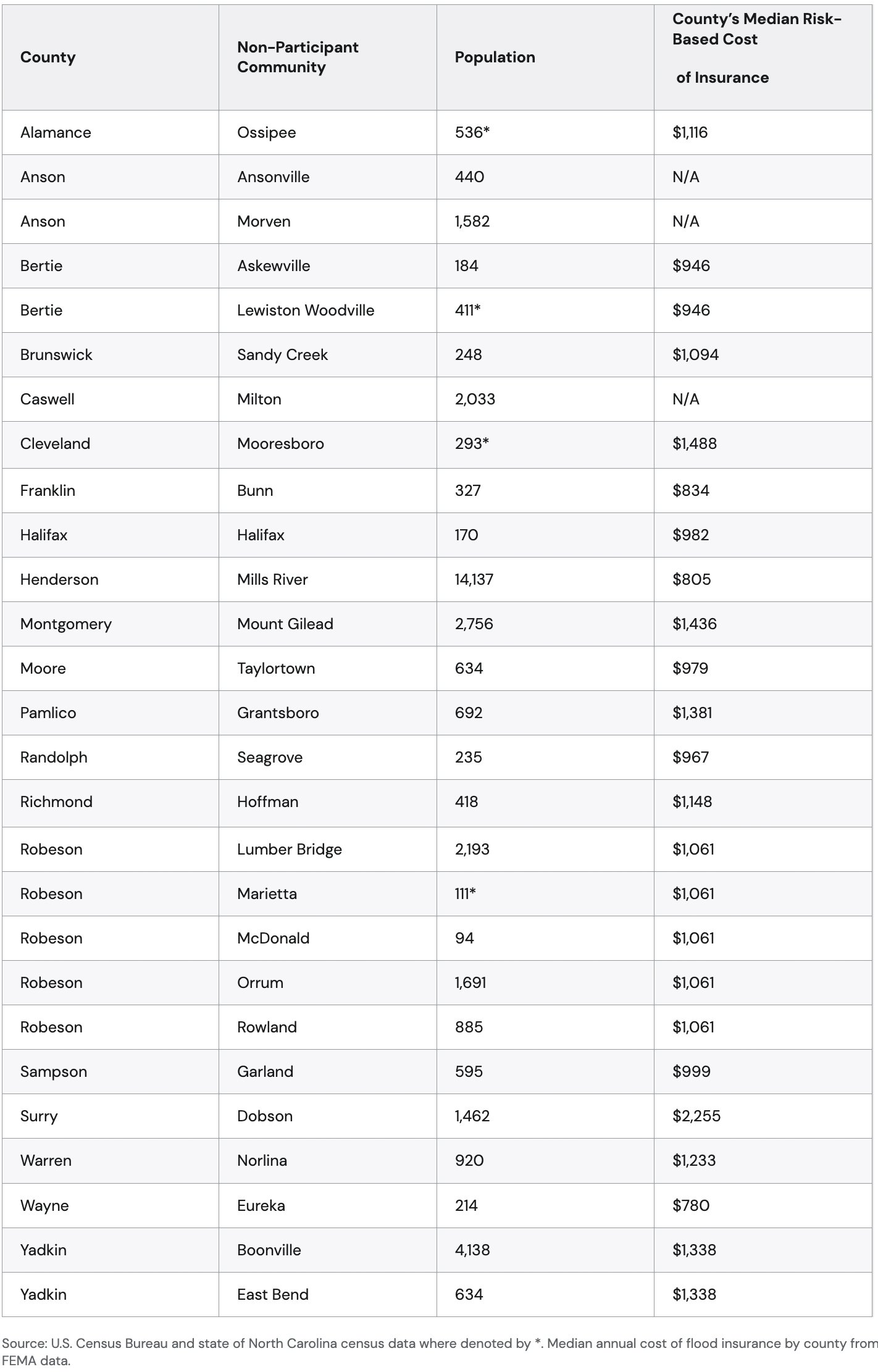

Insurify

What’s Next: Will Communities Rethink Non-Participation?

Table showing information on non-participating communities.

Helene’s severe effect on many inland communities across multiple states took many people by surprise. But with climate change driving more frequent and stronger hurricanes and other weather events, it’s likely more communities will face situations similar to Helene’s effect on Western North Carolina.

Smaller communities may be unaware of the elevated risks they face.

“In counties and rural areas, you need to pick up 10 to 20 square miles of drainage before a FEMA flood map starts picking up on the floodplain area, yet you have flood risk even if there’s only a square mile of drainage,” Berginnis said. “These small communities way up in the hollows, they have significant flood risk. [But] we’ve not mapped it, and that’s, I think, on us as a country.”

Property owners can take steps to protect themselves, even if they’re in a non-participating community, he said. The federal government has been working for over a decade to support the development of a private flood insurance market. People in communities where NFIP coverage isn’t available may be able to purchase private flood insurance. Homeowners and businesses can also ask their town leaders to begin participating in the NFIP.

Above all, Berginnis cautioned, communities should continue to prepare for flooding—even those that have already experienced a catastrophic flood event.

“Do not delude yourself to think it can’t happen again, or it won’t happen again. It will,” he said. “And it could happen next week, it could happen next month, it could happen a year from now—the same extreme event.”

This story was produced by Insurify and reviewed and distributed by Stacker.