Consumers with 1 credit card have lower debt and better credit, on average

New Africa // Shutterstock

Consumers with 1 credit card have lower debt and better credit, on average

A single card inside a green wallet.

Minimalism has been sparking joy for more than a decade. Multiple international bestsellers and Netflix productions on decluttering, along with plenty of TikToks, all suggest that the multibillion-dollar less-is-more industry is more than a passing fad. With that in mind, Experian explored what exactly the financial version of minimalism might look like.

We looked at aggregated data of consumers with only one active credit card to see how these consumers are faring with credit, where these financial minimalists are and how they’re managing their debt. Having a single credit card may seem constraining, but Experian data shows that most consumers with only a single card are doing more than OK.

![]()

Experian

One Isn’t the Loneliest Number After All

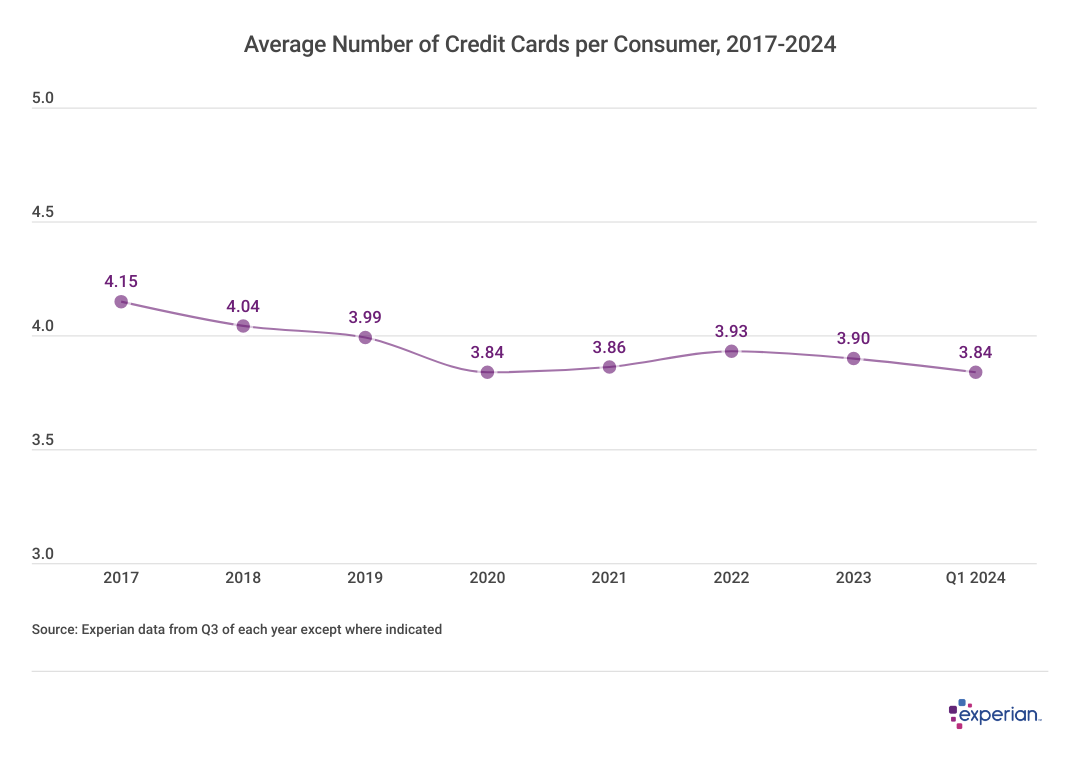

[Line graph “Average Number of Credit Cards per Consumer, 2017-2024”]

Most U.S. consumers have at least one credit card, though the average consumer has about four active credit cards, a figure that’s been largely unchanged for a number of years. The vast majority of these cards are general purpose credit cards, which simply means that they can be used anywhere that card is accepted. However, some store credit cards, which can only be used in particular stores, are also part of this average.

However, that average doesn’t mean that having four credit cards in your wallet, virtual or otherwise, is the norm. In fact, consumers with just one bank card to their name are quite common, as 25% of consumers use just a single card as of the first quarter (Q1) of 2024, according to Experian data.

Experian

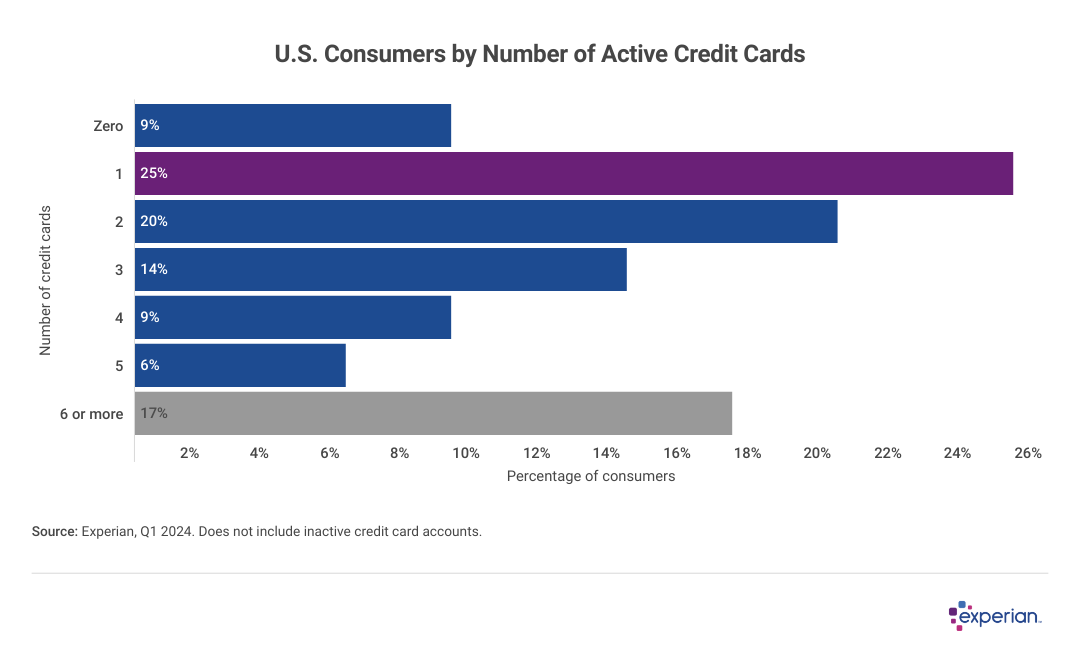

Single Card Users Have Higher Average Credit Scores and Lower Balances

Bar graph showing results for “U.S. Consumers by Number of Active Credit Cards”.

As one might expect, average balances of consumers with a single credit card are generally lower than total balances of all consumers. The average balance of $2,134 for single credit card borrowers is about one-third of the size of the U.S. average credit card balance of $6,541. Credit usage differs as well among one-card consumers, who only owe an average of 21% of their total credit limit, versus 29% for all consumers.

It may also explain why the average FICO Score of these single card users is slightly higher. Those with a single active account have an average FICO Score of 718, versus 715 for all consumers, as of Q1 2024, according to Experian data.

Experian

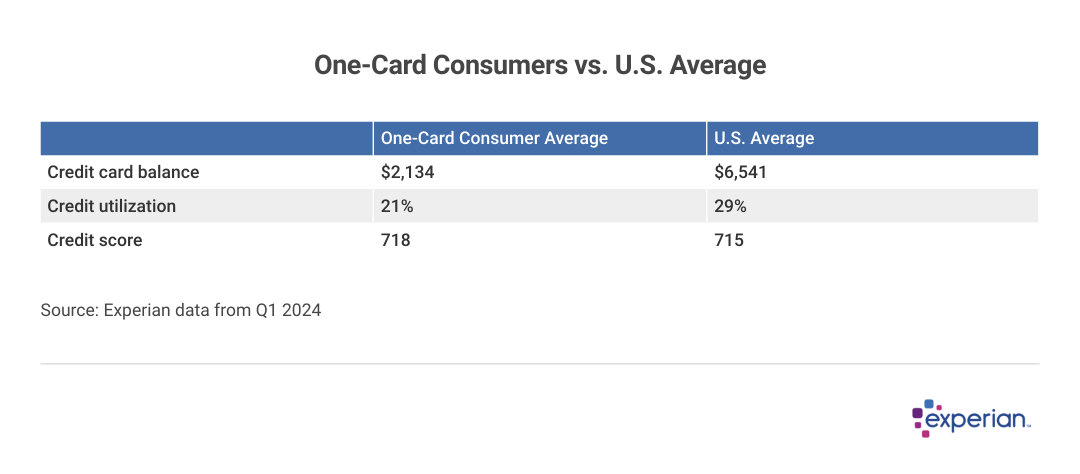

Many Consumers With One Credit Card Are Younger

Table showing “One-Card Consumers vs. U.S. Average”.

It’s tempting to hypothesize that the reason some consumers only have one credit card isn’t so much of a choice as much as a temporary state of affairs until they apply for and receive a second card. While that’s certainly the case for some consumers, particularly younger ones, some more established consumers are apparently making a choice to use just one card.

Experian data shows that a sizable portion of every generation carries just one card. Having one card is more common among Gen Zers, but single card use is still prevalent deep into middle age, when consumers tend to have more financial balls in the air than in other times of their lives.

Experian

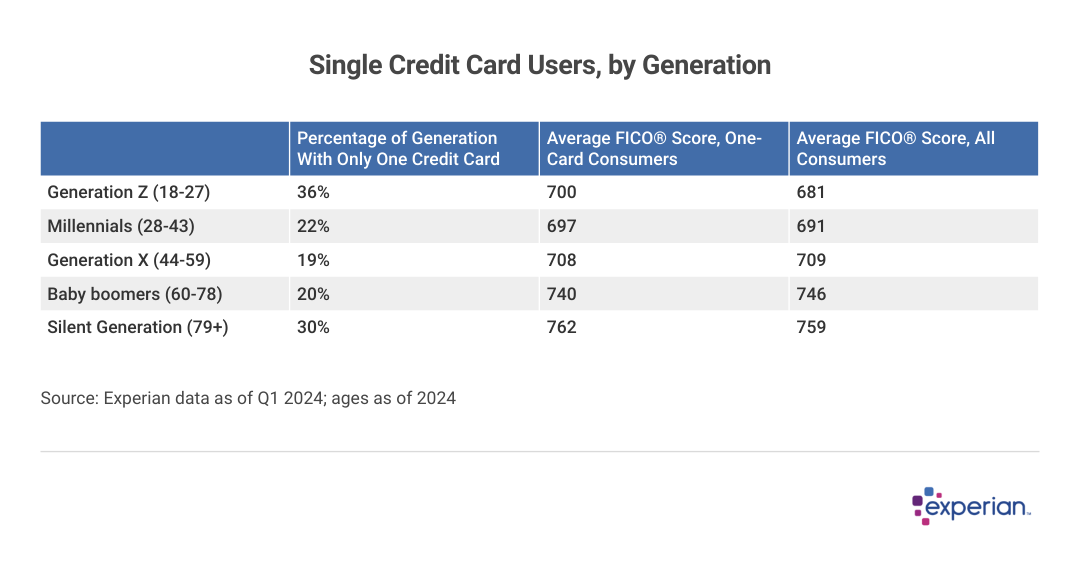

The Single-Card Habit Is Everywhere

Table showing comparisons for “Single Credit Card Users, by Generation”.

Less-than-stellar credit may be part of the reason some of these consumers either don’t want or don’t receive offers for new credit, but average FICO Scores of single-card users aren’t appreciably different than other consumers (if anything, there’s less variance among their scores, as we illustrate below).

In other words, if this generational pattern holds, we can expect more than some of the 36% of Gen Zers with only a single card to manage to remain that way as we all move through the decade.

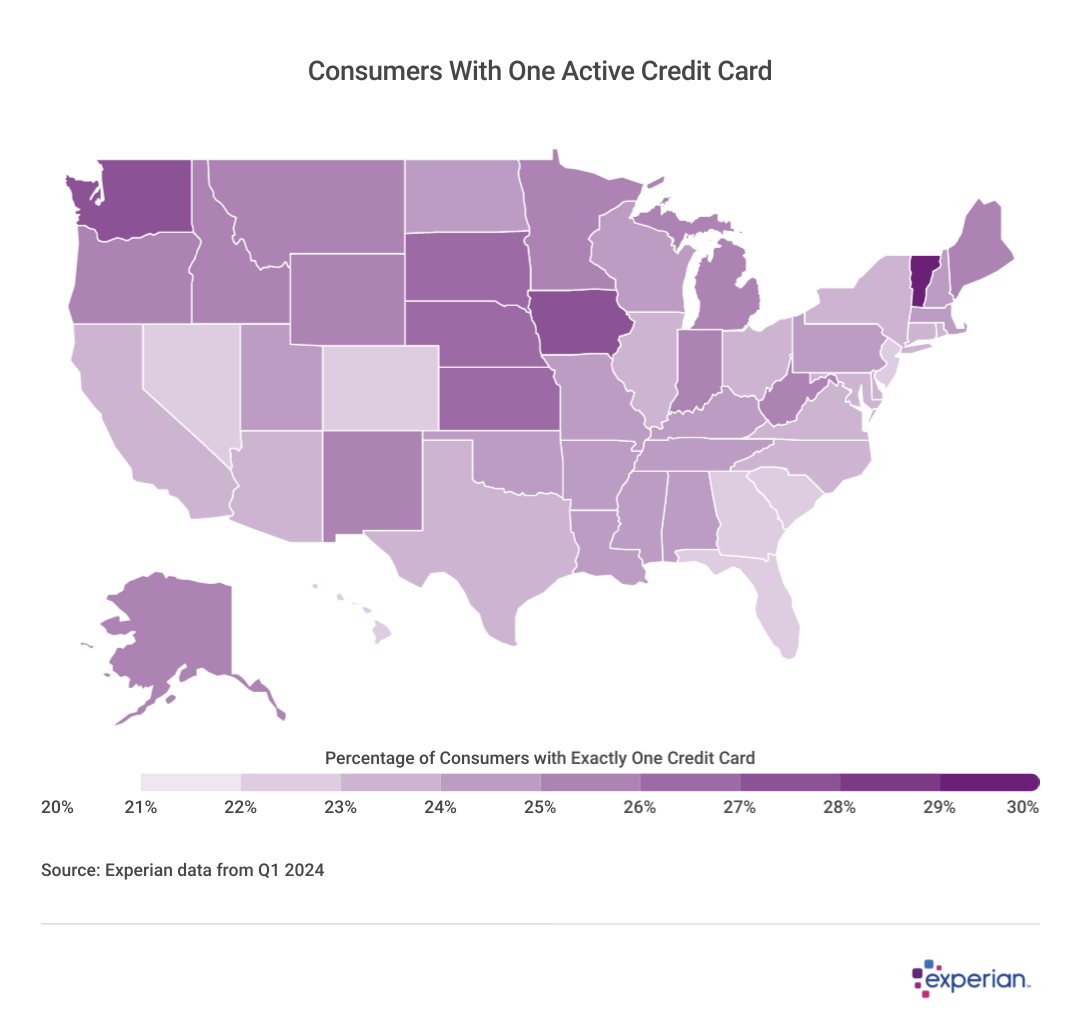

Experian’s data suggests there’s no particular regionality among the number of credit cards in a wallet: No state varied more from the national average of 25% by more than 4 percentage points. Vermont wins the crown for most minimalist wallet, with 29.2% of consumers there only having one card account.

Experian

Not Much Variance in Credit Scores

Heatmap showing states results for “Consumers With One Active Credit Card”.

Drilling down, the credit scores of consumers with only one credit card aren’t necessarily higher or lower than consumers with more credit cards—or those with none at all. However, their average FICO Scores appear to vary far less than the population at large. For example, while average FICO Scores at the state level range from 680 to 743 as of Q1 2024, the range in average FICO Scores is much narrower—ranging from a 700 to 739 FICO Score—when just examining consumers using only a single card.

Easier to Handle One Card

Possible explanations include fewer delinquencies on these consumers’ credit reports, as Experian data shows, instead of the average of four or more. In addition, as previously mentioned, they also have lower utilization rates than consumers at large.

Regardless, although having a single card card doesn’t necessarily improve your credit, those with a single credit card are more likely to be Steady Eddies versus other consumers: A higher percentage of one-card consumers have good credit scores, and a lower percentage have poor scores.

Balance Transfer Offers Can Help Reduce the Number of Cards You Carry

If you have more than one credit card with a balance and want to consolidate all those monthly payments and save on interest in the process, then a balance transfer credit card offer is one way to do it.

Typically, balance transfer offers allow you to transfer interest-accruing balances from other credit cards to the new balance transfer card, with the transferred balances not being charged interest for a number of months (often 12 to 21 months). Borrowers may still have to pay a balance transfer fee amounting to 3 to 5% of the balances transferred.

Of course, you’ll need a reasonably good credit score to receive better balance transfer offers, and a missed payment can quickly restart the interest-accruing meter on the transferred balances. But those who can stick to a plan of reducing those transferred balances may not only have bought themselves some extra time and savings, but also more room in their pocket free of excess plastic.

Methodology: The analysis results provided are based on an Experian-created statistically relevant aggregate sampling of our consumer credit database that may include use of the FICO Score 8 version. Different sampling parameters may generate different findings compared with other similar analysis. Analyzed credit data did not contain personal identification information. Metro areas group counties and cities into specific geographic areas for population censuses and compilations of related statistical data.

This story was produced by Experian and reviewed and distributed by Stacker Media.