It's never too late to plan ahead: Here are the major milestones on the road to retirement

Canva

It’s never too late to plan ahead: Here are the major milestones on the road to retirement

An older woman in a cardigan sweater stands on a beach with her arms raised

Everyone has their own unique retirement timeline, needs, and strategies. But thanks to factors like Social Security, Medicare, and IRS rules, just about everyone will face retirement planning milestones in approximately the same order and at the same stage in life.

Wealth Enhancement Group outlines the major milestones you’ll face in retirement and the ages at which you’ll face them—starting with right now.

Navigating your journey to retirement is much easier with a financial advisor at your side. While you can partner with an advisor at any stage of your life, choosing one sooner rather than later is best. Your advisor can then help you evaluate your situation, plan for these milestones, and get you through your retirement years with your best interests in mind.

![]()

Wealth Enhancement Group

In your 40s

A graphic showing retirement milestones in your 40s

Max out your retirement accounts

You need to save a lot of money for retirement—especially in your peak earning years. This is a time when you’re likely benefitting from an employer-sponsored health plan, and you may even be enjoying a hard-earned break from the expenses of raising and educating children. Take advantage of it by contributing as much as possible to your retirement accounts.

Make Roth IRA contributions

There are limits to how much you can contribute to your Roth IRA. In 2023, if you’re under age 50, you can only contribute up to $6,500 for the entire year. If you’re over 50, you can contribute an extra $1,000 in catch-up contributions.

Even then, the amount you can contribute is dependent on your income. Once you reach a certain limit, the amount you can contribute starts to phase out. Contributing to your Roth IRA early allows for longer tax-free growth and ensures you don’t lose the opportunity to make contributions.

Start building tax diversification

Tax diversification is intentionally distributing your assets between various investment accounts that are taxed differently. Just like you should have diversification in your investments, you should also have diversification in how your retirement accounts are taxed.

Essentially, this means you should start spreading your assets around various accounts that are taxable, tax-deferred, or tax-advantaged. This strategy allows a more even distribution of your tax burden throughout your life by allowing you to vary what sources you draw income from based on your circumstances.

Wealth Enhancement Group

In your 50s

A graphic showing retirement milestones in your 50s

Make a plan for long-term care

It’s estimated that 7 out of 10 people will require long-term care (LTC) at some point in their lives, so you’d be wise to plan how you can pay for it, should you need it. You could pay for it on your own or look into LTC insurance, which can help you pay for services generally not covered by Medicare. If you decide to go the LTC insurance route, your early 50s are a great time to start. The older you enroll, the higher your annual premiums will be.

Catch-up contribution eligibility begins at age 50

There are limits to how much you can contribute to your various retirement accounts each year. However, once you turn 50, the IRS allows you to contribute an additional amount on top of the existing limits, called “catch-up contributions.” These get adjusted annually, so keep an eye out for them.

Early, penalty-free withdrawals from 401(k)s may begin at age 55

Under certain conditions, it’s possible that you can start taking withdrawals from an employer-sponsored 401(k) account without incurring the 10% early withdrawal penalty fee. However, it would help if you retired in the year you turn 55, and you can only take these penalty-free withdrawals from a 401(k) account that’s sponsored by the employer you’re leaving. Additionally, it’s only recommended that you start taking these withdrawals if absolutely necessary. Your advisor can help you devise a withdrawal strategy that works for you.

Penalty-free withdrawals from all retirement accounts beginning at age 59½

You can start withdrawing from all qualified retirement accounts and IRAs at this age without incurring the 10% penalty fee. However, those withdrawals may still be taxed as regular income, depending on the account.

Wealth Enhancement Group

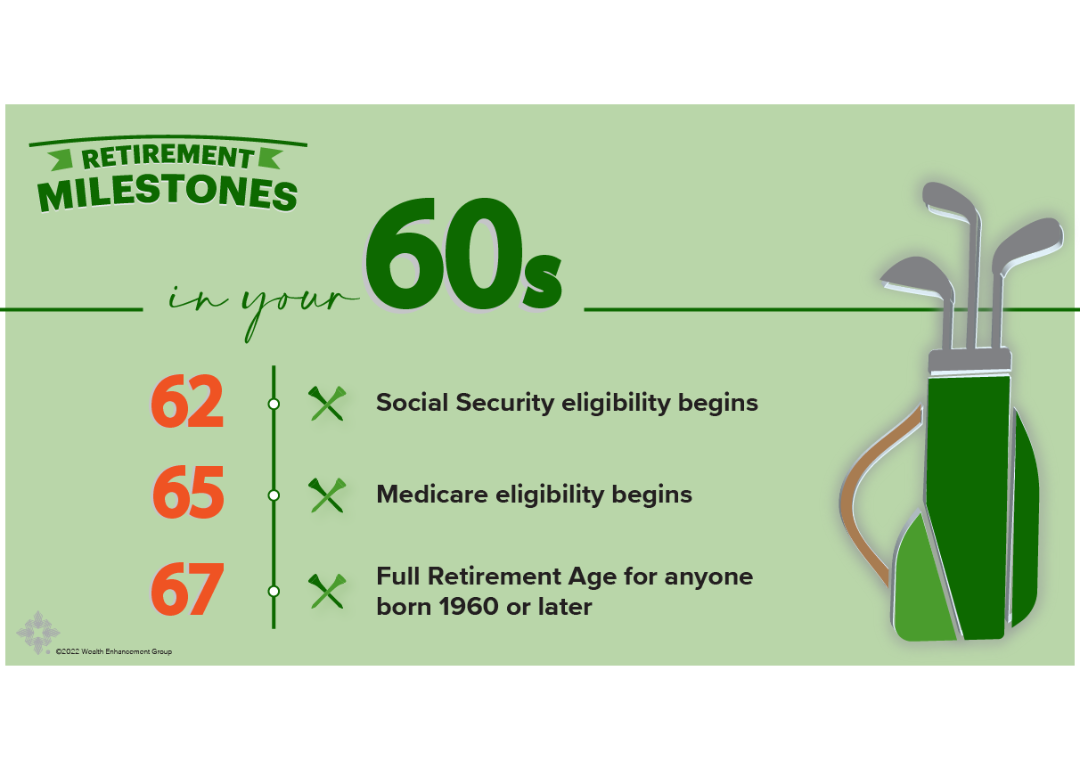

In your 60s

A graphic showing retirement milestones in your 60s

Nail down your retirement plans

People typically retire in their 60s, so if this sounds like you, make sure you plan for it and set a date. Then, book that trip, spoil those grandkids, and do what makes you happy. You earned it.

Consider doing Roth conversions

After you retire but before you start drawing Social Security—and before required minimum distributions (RMDs) kick in—it can be an excellent time for Roth conversions. The thinking here is that you have less income after you retire, so you should be in a lower tax bracket and will be taxed less on your Roth conversion. A financial advisor can help you determine if Roth conversions make sense for your situation, when, and how much.

Social Security survivor benefits may be available at age 60

If your spouse dies, you can start claiming off their Social Security benefit at age 60. How much you’re entitled to depends on a few factors, but it will be at a reduced amount. However, once you turn 62 and are eligible for your own Social Security benefit, you can switch to the higher monthly benefit amount.

Social Security eligibility begins at age 62

At this age, you can begin drawing from your Social Security benefit, albeit at a permanently reduced amount—monthly payments will be approximately 75% of your full benefit.

Medicare eligibility begins at age 65

This is when most Americans are eligible for Medicare. However, Medicare comes in four segments (Parts A, B, C and D), so educate yourself on what you’re getting into and what you’re signing up for. You must also make some sort of election once you’re eligible for Medicare; if you don’t, you could be permanently penalized.

Social Security full retirement age at 66 or 67 (depending on when you were born)

Full retirement age (FRA) refers to the age at which you are eligible to receive 100% of your Social Security benefit. For those born between 1955 and 1959, FRA is 66 plus two months for each year you were born after 1954 (so, if you were born in 1957, your FRA is 66 years and six months). For those born in 1960 or later, FRA is 67.

Wealth Enhancement Group

In your 70s

A graphic showing retirement milestones in your 70s

Ensure your estate plan is in order

While it’s a good idea to have your estate plan in place well before you reach your 70s, the older you get, the more critical it is to ensure your ducks are in a row. Five key documents/legal entities are essential in any good estate plan (like your will, beneficiary designations, power of attorney, etc.), so make sure you have them all in order and review your estate plan regularly. A financial advisor can work closely with your attorney to ensure all aspects of your finances are addressed in your estate plan.

Your last year to claim Social Security is age 70

Not only is age 70 the final year you can claim your Social Security benefit, but it’s also the age at which you can receive the maximum monthly benefit amount. Your Social Security benefit increases by about 8% annually between FRA and age 70, so if you can wait until you turn 70 to start claiming, you can receive 132% of your full Social Security benefit.

Qualified charitable distribution eligibility begins at age 70½

Qualified charitable distributions (QCDs) are direct transfers of funds from your IRA to a qualified charity. These can be counted towards your annual RMDs and keep your taxable income lower.

RMDs kick in at age 72

At this age, you have to start taking distributions from qualified retirement accounts like 401(k)s, 403(b)s and Traditional IRAs. RMDs are counted towards your taxable income, so planning for them is essential.

This story was produced by Wealth Enhancement Group and reviewed and distributed by Stacker Media.