Buyer beware: Unregulated 'buy now, pay later' loans can lead to greater debt and higher costs for you

Przemek Klos // Shutterstock

Buyer beware: Unregulated ‘buy now, pay later’ loans can lead to greater debt and higher costs for you

Mobile app showing a buy now pay later transaction

America’s debt addiction takes on a new twist—thanks to opaque, unregulated “buy now, pay later” loans that have swept retail in the past few years.

There’s no single definition of a BNPL loan, but it usually refers to a point-of-sale loan that shoppers can pay off in smaller increments, often under the promise of interest-free payments.

“BNPL is a pretty slick innovation. It is convenient and it’s basically free credit if you pay it off on time,” said Ed deHaan, a professor of accounting at Stanford Graduate School of Business.

BNPL may be a “slick innovation,” but it’s also wrought with misuse, so much so that it’s landed on the Federal Reserve’s radar.

According to a recent Fed report, BNPL loans can take advantage of financially fragile households by offering them lending products they don’t fully understand—and that eventually end up costing them more. Creditnews explores the growing trends in “buy now, pay later” loans and how one state is fighting for regulation.

![]()

Creditnews

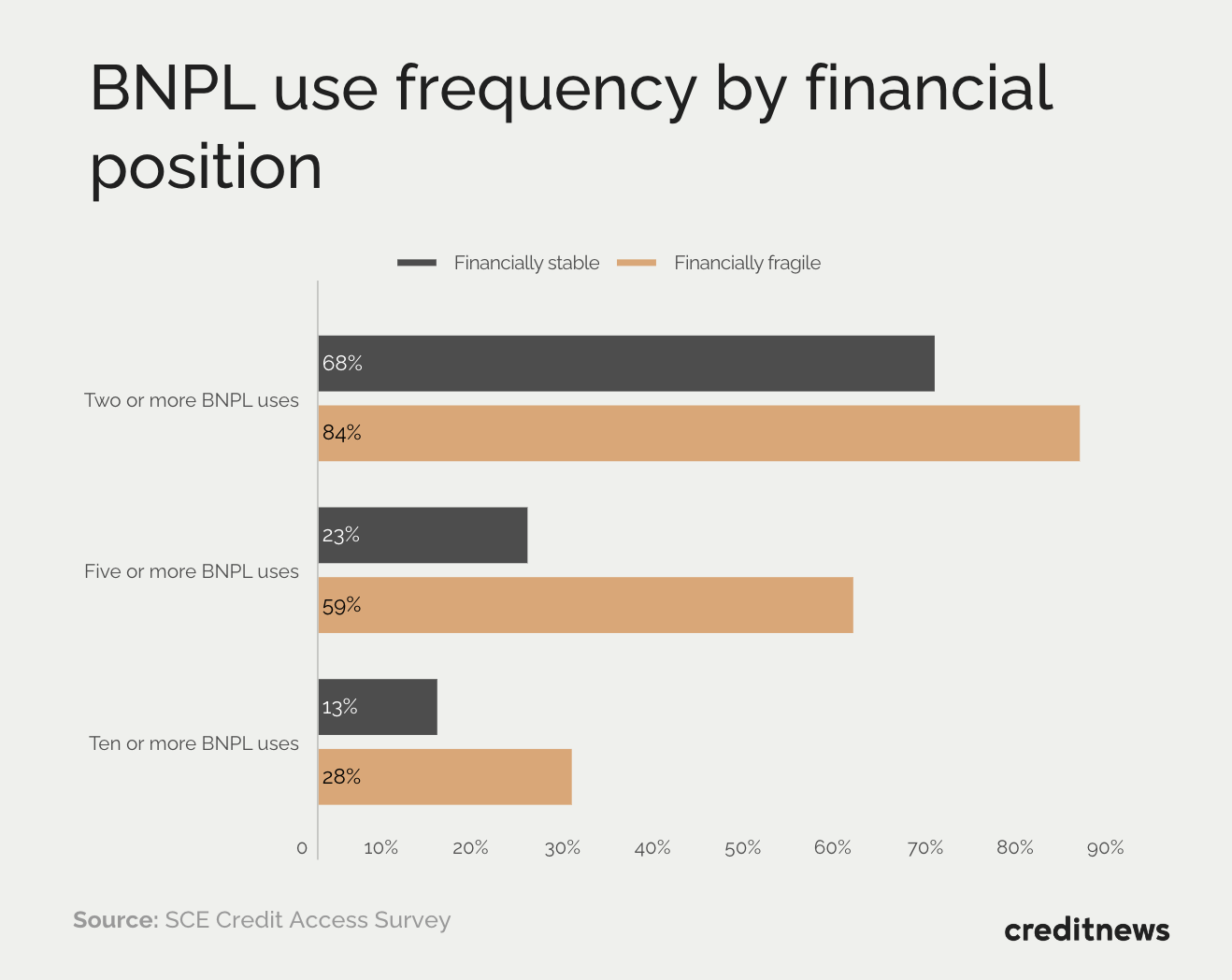

Financially fragile consumers more likely to use BNPL loans

Chart showing BNPL use frequency by financial position

Although a BNPL loan is a relatively new and still unregulated product, it’s no longer as niche as many think.

As of December 2022, one in five Americans had taken out a BNPL loan, according to Consumer Reports, a New York-based advocacy group.

Experts believe the global BNPL market could reach $1 trillion by 2025. That’s nearly as much as America’s total credit card debt, which surpassed the $1 trillion mark at the end of last year.

But while BNPL can be useful convenience for one shopper, for many others it’s a gateway into more, possibly unaffordable, debt.

Creditnews

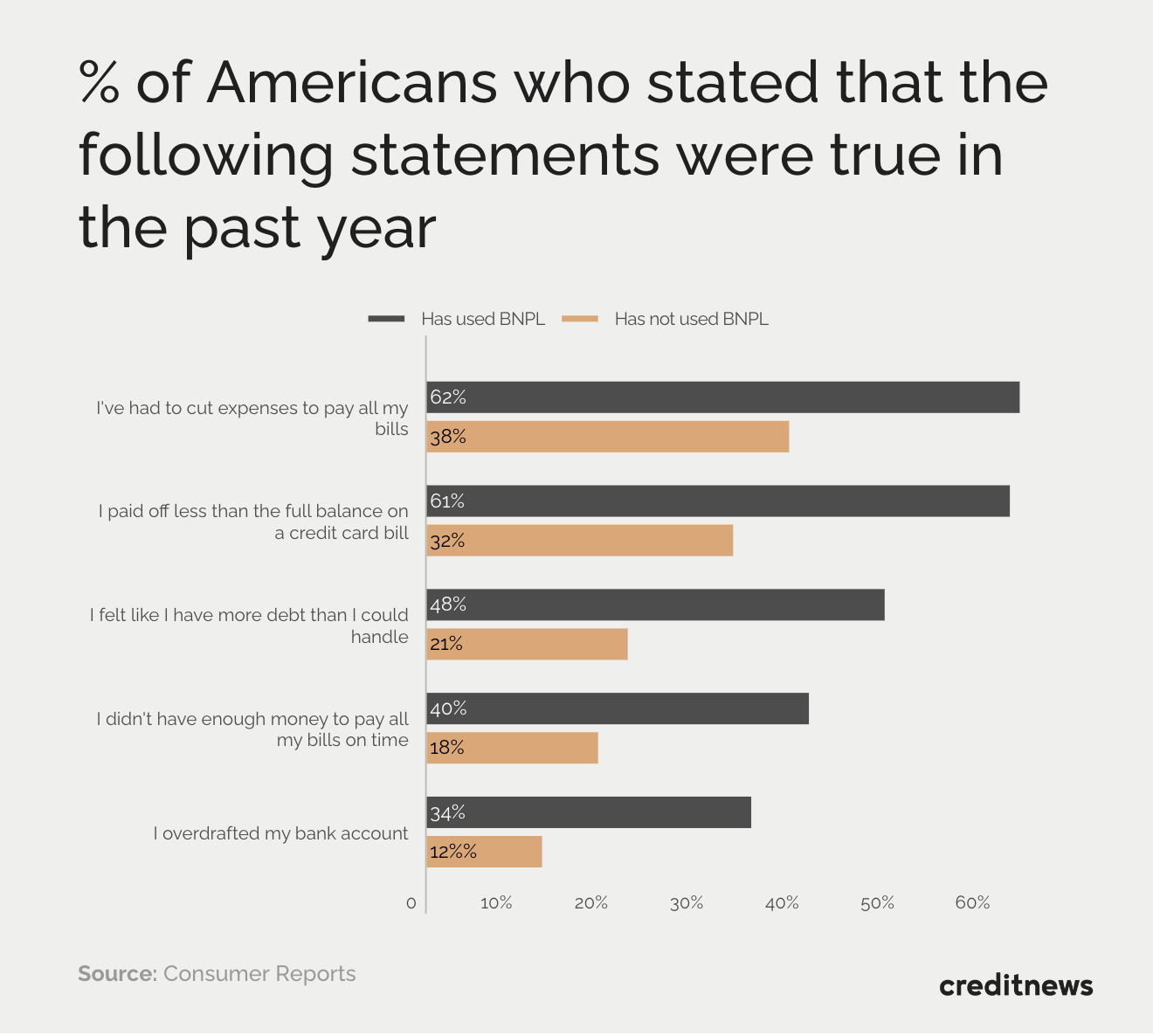

Buy now, pain later

Chart showing % of Americans who stated that the following…

The rise of BNPL personal loans is a textbook tale of “haves” versus “have-nots.”

The same New York Fed report found that financially insecure Americans are much more likely to resort to BNPL. In fact, these borrowers are up to three times more likely to take out these loans than their financially stable peers.

A survey from Consumer Reports also found a strong connection between BNPL use and financial setbacks.

Survey respondents who’d had to cut expenses to pay bills, couldn’t pay off their credit card balance, or had another financial strain were far more likely to use BNPL loans than those who didn’t.

Creditnews

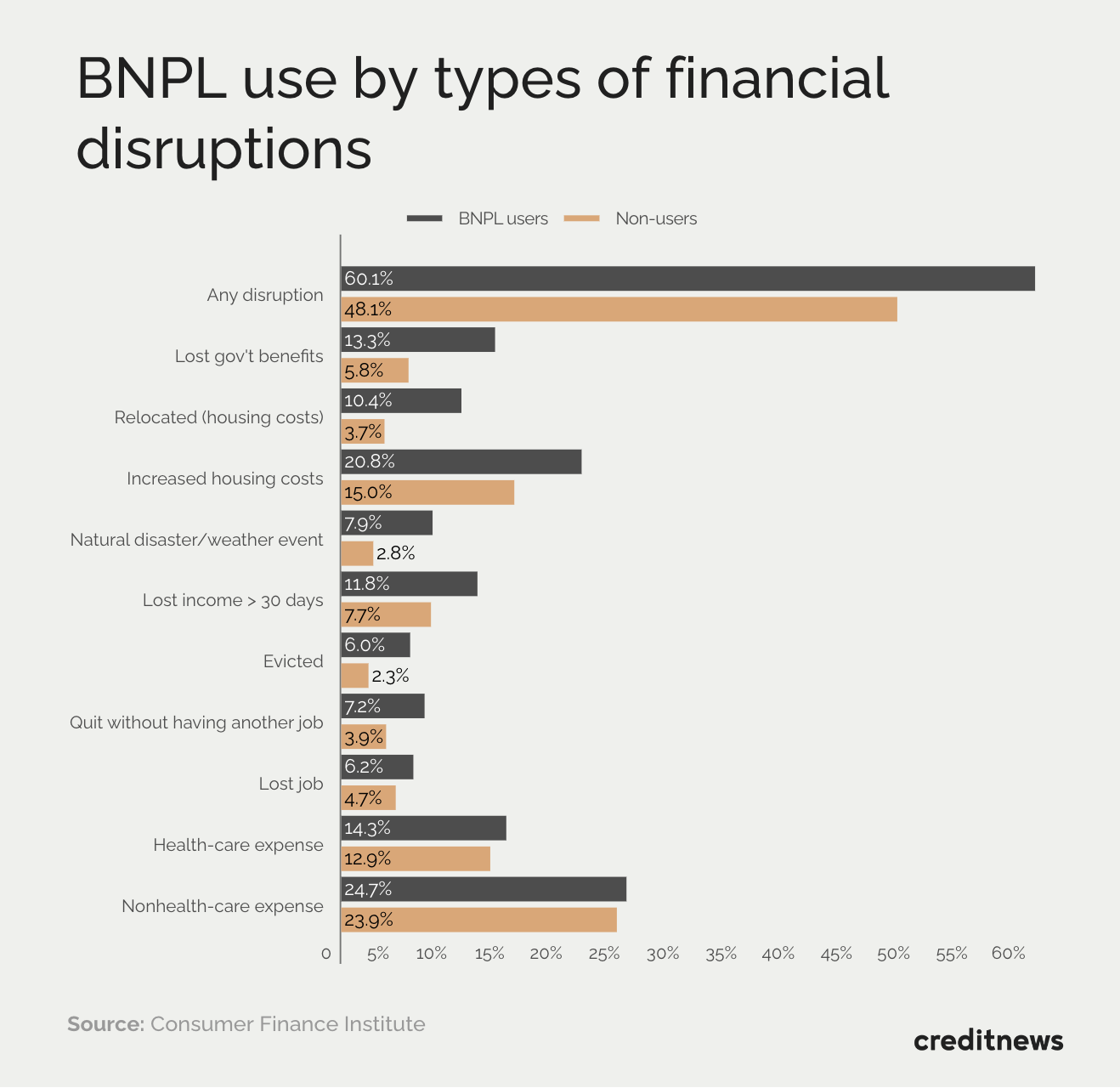

Top reasons why consumers resort to BNPL financing

Chart showing BNP use by types of financial disruption

In fact, 60% of BNPL users had experienced a “financial disruption” in the last 12 months, compared with 49% of non-users, according to a report released by the Consumer Finance Institute (CFI).

Equally as important, “More users than non-users report concerns about their ability to make their monthly payments within the next 12 months,” report authors Tom Akana and Valeria Zeballos Doubinko wrote.

Perhaps the most significant aspect of BNPL loans is that the industry didn’t even exist before 2019.

The Empire State strikes back

Inherent BNPL risks now have lawmakers and financial watchdogs scrambling to regulate this market.

In January, New York Governor Kathy Hochul put forward new legislation intended to establish “strong industry protections” and force BNPL operators to obtain a license before operating in the state.

The proposed legislation would also give the New York State Department of Financial Services (NYSDFS)—one of America’s most feared watchdogs—full authority to regulate and supervise the industry.

Although definitions of “buy now, pay later” lending can be fuzzy, the legislation would cast the net as wide as possible to include any service that extends credit to consumers to purchase goods and services, excluding a motor vehicle.

According to global law firm Steptoe LLP, “The proposal appears to capture all forms of point-of-sale financing, including, arguably, credit cards.”

While New York is leading the charge to regulate BNPL at a state level, much of its guidance comes from the Office of the Comptroller of the Currency (OCC), which oversees the entire U.S. banking system.

In a December bulletin, the OCC identified several major risks BNPL lending poses to banks and consumers.

“The lack of clear, standardized disclosure language could obscure the true nature of the loan, result in consumer harm, or present potential risks of violating prohibitions on unfair, deceptive, or abusive acts or practices.”

Meanwhile, the Consumer Financial Protection Bureau has taken matters into its own hands.

The CFPB’s director, Rohit Chopra, previously instructed his staff to monitor the sector and identify “interpretive guidance” that may apply to it—including observing how BNPL lenders gather data.

While not evident yet, BNPL lending is likely to become much more regulated in the very near future.

This story was produced by Creditnews and reviewed and distributed by Stacker Media.