Total mortgage debt increased to $11.2 trillion in 2022

Canva

Total mortgage debt increased to $11.2 trillion in 2022

Aerial view of a residential neighborhood with homes.

When 2022 began, there were more real estate agents than homes for them to sell. And that was before the Federal Reserve started raising interest rates, which further tightened an already-thin housing market. By the end of 2022, existing home sales were down by 37%. Some markets, including Las Vegas and Phoenix, saw sales fall by two-thirds.

What few homes remained in the nation’s inventory were subsequently priced much higher than in the previous year, based on various home price indexes: Federal Housing Financing Agency (FHFA) data indicates that home prices increased by 12.4% nationwide as of the third quarter (Q3) of 2022, while the S&P/Case-Shiller U.S. National Home Price Index was up 10.7%.

So it follows that those who borrowed to make home purchases in 2022—about two-thirds of all buyers—would assume higher mortgage balances to make their purchases. Both home scarcity and mortgage rate increases fueled the increases in balances.

Overall Mortgage Debt

- 2020: $9.56 T

- 2021: $10.29 T

- 2022: $11.22 T

- 2021-2022 Change: +9%

The 9% increase in overall mortgage debt, while not quite as large as the home price increase over the same period, was still enough to add nearly $1 trillion more to the overall debt balance.

As part of its look at consumer credit and debt trends in 2022, Experian examined the reasons behind the decline in the number of new mortgages created and why balances are increasing.

![]()

Experian

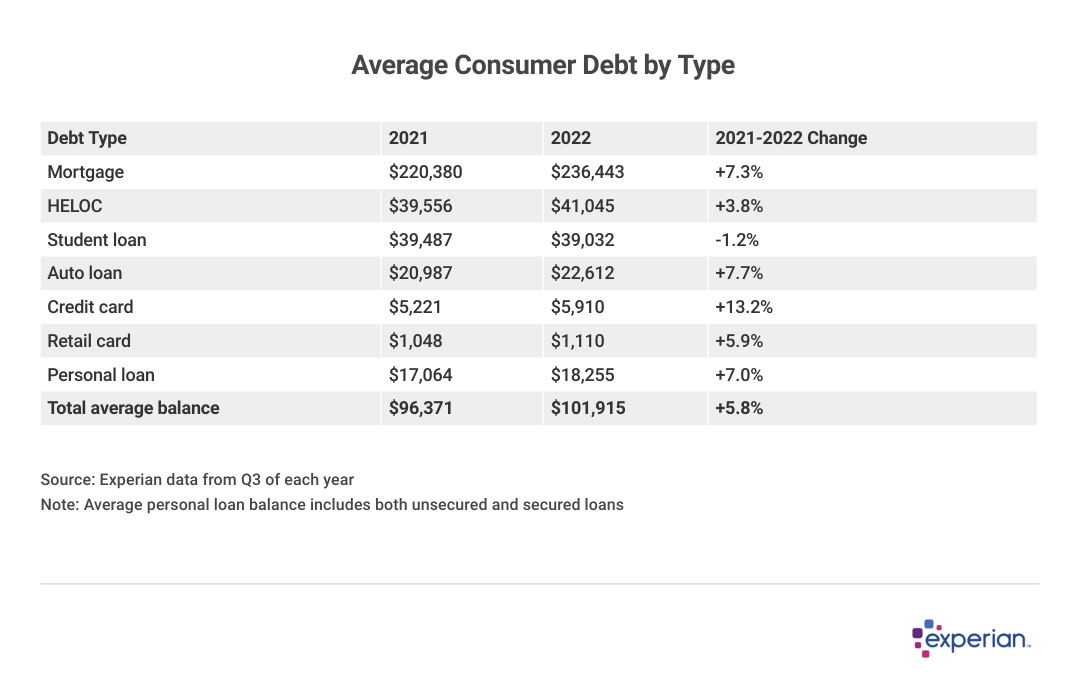

Average Mortgage Debt Increases by 7.3% in 2022

Table showing average consumer debt by type.

New mortgages—nearly all of which sport higher APRs and higher monthly payments than older mortgages—increased the average mortgage balance to $236,443 in September 2022, a 7.3% rise from September 2021.

For the second consecutive year, the average mortgage balance increased by more than $10,000. The increase of 7.3%, or $16,063, exceeded the 2021 increase of 5.9%. But that doesn’t mean the housing market was red hot. On the contrary: 2022 was the year the housing market began to contract, resulting in a market of fewer sellers and buyers:

- Throughout 2022, fewer homes were sold than in the month prior, according to the National Association of Realtors.

- Home listings, which were already scarce for a number of years, fell below 1 million units for much of the year; historically there are at least twice as many homes listed.

- Sharp mortgage rate increases discouraged buyers who were unable to afford increases in both price and financing costs.

Experian

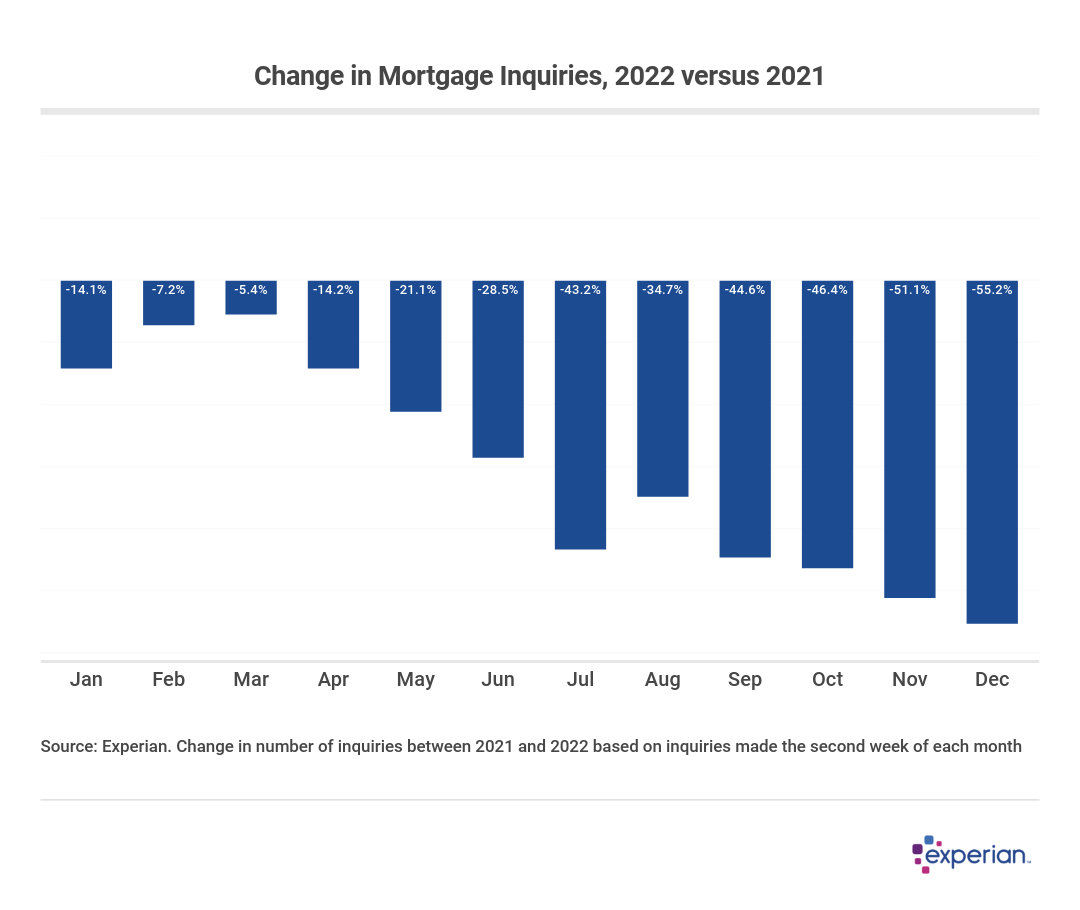

Mortgage Inquiries Decline as Borrowing Rates Increase in 2022

Bar chart showing change in mortgage inquiries from 2022 versus 2021.

There’s no sugarcoating it: The mortgage market largely disappeared once rates began to increase at the beginning of 2022. Mortgage inquiries were already declining in late 2021, as most borrowers who needed to refinance their mortgage had already done so.

A credit inquiry is added to a consumer’s credit file when they apply for credit with a lender, and credit inquiries related to mortgages indicate how many consumers applied for a mortgage during a certain period of time. With fewer home listings appearing every month, and fewer buyers with the ability and appetite to purchase them, the number of new mortgage inquiries decreased significantly. Home prices—and the size of new mortgages—continued to increase throughout the year in most markets.

As rates on 30-year mortgages rose from 3% to more than 6% in a matter of months, not only were there few remaining borrowers who could benefit from refinancing an existing mortgage, but some prospective homebuyers were kept out of the pool as well.

Experian

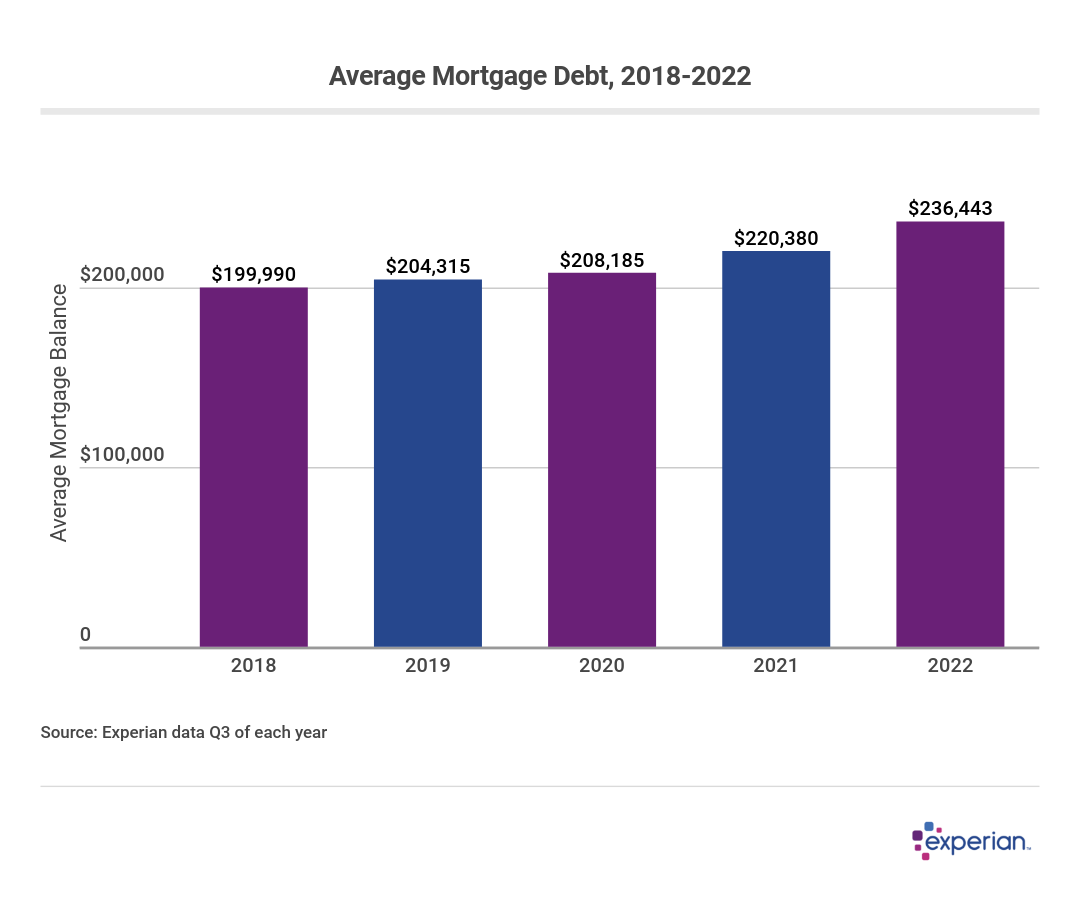

Average Mortgage Balances Increase More Than $16,000 in 2022

Bar chart showing average mortgage debt from 2018 to 2022.

The increase in average mortgage debt to $236,443 was the largest jump in recent years. As with other forms of consumer financing, the drivers of this increase included rising borrowing rates for consumers, shortages of existing homes for sale, suppressed new construction and the inflation that follows when there’s much more demand than supply.

Compared with other types of consumer debt, average mortgage balances increased more than personal loans and student loans, but less, in percentage terms, than auto loans and credit card balances. Nonetheless, the more than $16,000 increase in average mortgage balance is by far the largest dollar amount increase consumers assumed in 2022.

When the Federal Reserve raises rates, mortgage rates usually don’t move in lockstep as most APRs on variable-rate credit cards do; mortgage rate changes are usually more subtle. But 2022 was an exception: Mortgage rates grew more, in percentage point terms, than even the federal funds rate. The average rate for conventional 30-year mortgages grew from around 3% to more than 6.7% in 2022, according to Freddie Mac data, while the Fed raised rates from 0.25% in September 2021 to 3.25% by September 2022.

Experian

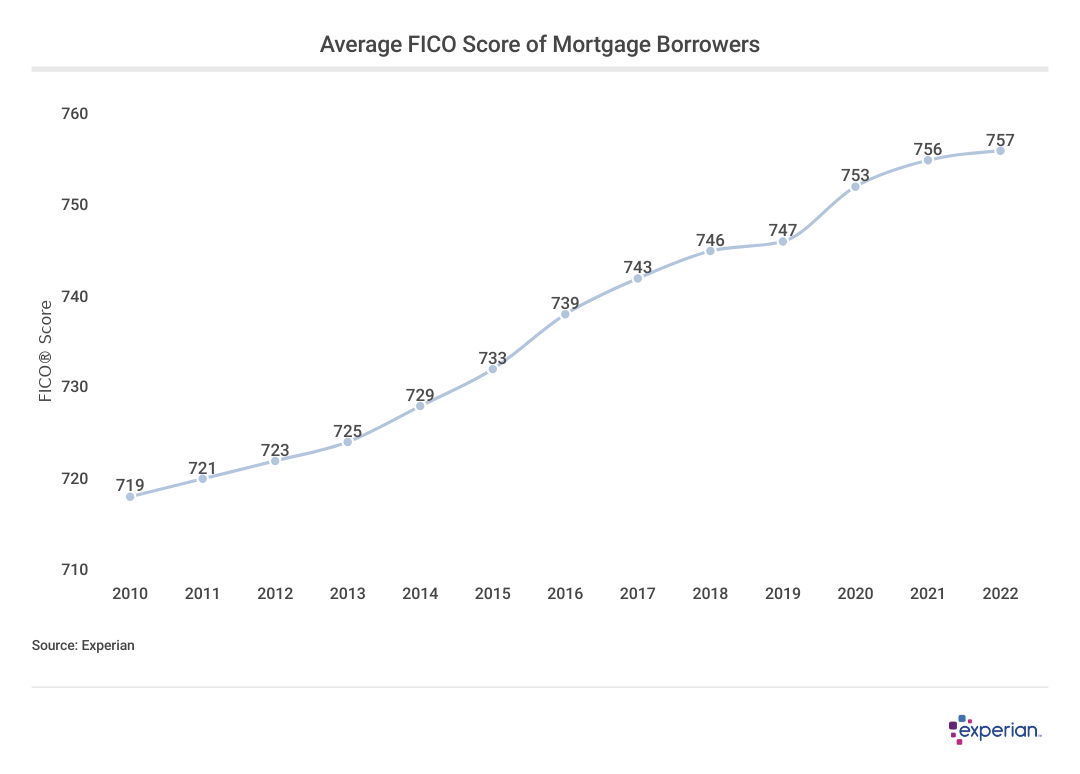

Average Credit Scores Among Homeowners Remain High

Line chart showing average FICO score of mortgage borrowers.

Average credit scores among homeowners may have plateaued, as mortgage holders sported an average FICO Score of 757 in 2022, a one-point increase from 2021.

While the flattening may be noteworthy, the journey there may be the larger story: Those with mortgages generally have been improving their credit scores over the past decade, indicating that overall these consumers are managing their mortgages and other debts well. (Also, the addition of a mortgage to one’s credit mix can help improve a borrower’s FICO Score.)

Millennials Now Carry the Highest Mortgage Balances

In 2021, millennial mortgage debt exceeded that of Generation X for the first time. In 2022, there’s even more daylight between the average balances of the two generations.

Although neither generation wants to hear it, the oldest millennials recently turned 42, and the oldest Gen Xers just turned 57. Despite the unsettled housing market, time marches on, and those millennials who want to own a home most likely bought recently via mortgage financing. Meanwhile, some of Generation X are possibly considering retirement, and may have paid down much of their existing mortgages.

For older generations, the beat goes on. Baby boomers and the Silent Generation saw slight increases in the relatively lower mortgage balances they may still have.

Experian

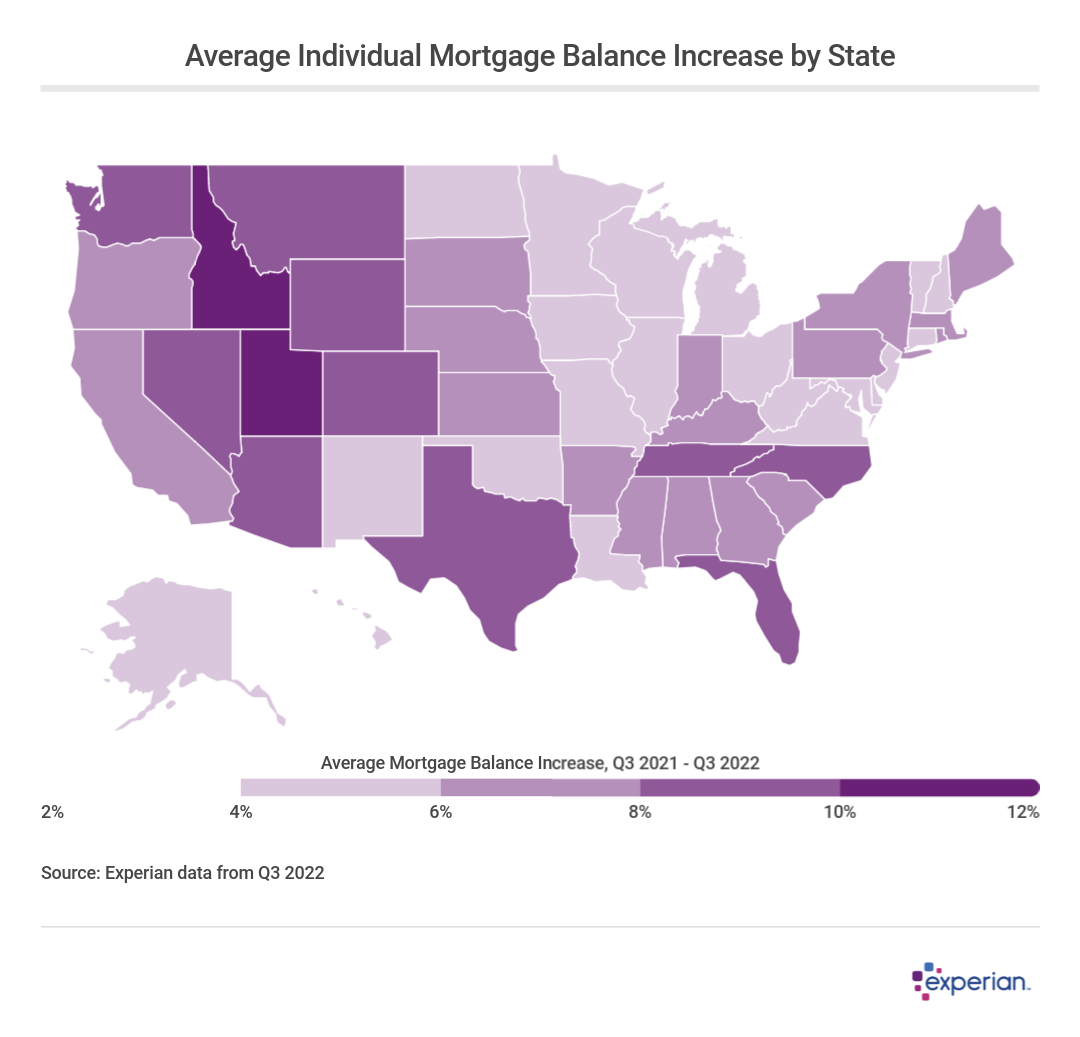

Mortgage Debt Increases Everywhere, but Most in the West

Heat map showing average individual mortgage balance increase by state.

Idaho, whose average mortgage debt balance increased 11.2% in 2021, saw balances grow another 12.6% in 2022 to lead the nation. But mortgage balances rose by at least 4% in every state last year. The differences among regions are more pronounced than in previous years.

Mortgage balances increased the most in Western states, with Idaho, Utah and Arizona showing the greatest increases. Despite the outsize increases in these states, average mortgage balances are still below $250,000, suggesting that consumers were willing to pay more to exit California’s sky-high housing market.

Mortgage balance increases in the South were more typical of the overall nationwide increase of 7.3%. Regional economic powerhouses like Florida, Tennessee and Texas saw above-average increases in 2022, while the more northern states in the South such as Delaware, Maryland and West Virginia saw more muted increases of around 4% from 2021.

In the Northeast, mortgage balances increased, but below the national average of 7.3% in every case. New York and Rhode Island grew the most, by 6.7%, while Connecticut saw the lowest increase in the country, with mortgage balances rising only 4% from 2021.

Usually the region of the country that aligns most closely with national mortgage balance averages, the Midwest showed some variance among its states in average mortgage balance increases. Only sparsely populated South Dakota saw balances increase more than the nation as a whole.

Canva

Outlook for Mortgage Borrowers in 2023

Two hands explore real estate options on a smart phone and a laptop.

With 2022 behind us, consumers, prospective homebuyers and current homeowners can expect to see a number of key housing metrics shift in 2023, as levels recede from the high-water marks reached in 2022.

Decreases in Some Home Prices

Home prices are already starting to decline in some markets, particularly in areas where they’ve been growing the fastest in recent years. As many as 20 local housing markets, most in the West where prices increased the most, fell in the last months of 2022.

A decrease in home prices, however, doesn’t equate to a housing crash. Even if prices fell by as much as 20%, that would simply return them to 2020 levels, as home prices increased by double-digit rates in nearly all markets over the past three years.

Nor would it necessarily mean an end to a severe inventory shortage: At least twice as many homes would need to be listed for sale than the 1 million homes currently on the market to approach a historically typical real estate market.

Modestly Higher Mortgage Delinquency Rates

Support for homeowners during the pandemic was largely dismantled in 2022, as mortgage forbearance programs and other offerings expired. Experian data shows mortgage delinquencies were at a historic low of less than 1% in 2021, before reversing course, hitting 1.46% in September 2022.

But even this rate is well below the long-term average delinquency rate for mortgages. Just prior to the pandemic, delinquencies were higher, at 2.2%, but even that was nowhere near the long-term average delinquency rate, never mind the above-average rates observed during economic downturns. But with the economy at or near full employment, most consumers are able to service any existing mortgages they may have.

More Types of Mortgage Financing

Mortgage products like adjustable-rate mortgages (ARMs) and mortgage buydowns weren’t used very often in the 2010s as conventional mortgages were available for nearly the same rate as ARMs, and borrowers didn’t feel a need to further reduce their mortgage rate with a buydown. But with typical mortgage rates hovering around 6% for much of 2022, some borrowers are employing these tactics to borrow for home purchases they might otherwise not be eligible for with a conventional fixed-rate mortgage.

More Home Equity Financing

Many homeowners are servicing other debts as well as their mortgages, and the price tag for some of those items, like auto loans and credit card balances, are rising as fast—if not faster— than home prices. Home equity loans and home equity lines of credit (HELOCs) allow some homeowners with enough home equity to borrow at lower rates than they might find elsewhere.

Methodology: The analysis results provided are based on an Experian-created statistically relevant aggregate sampling of our consumer credit database that may include use of the FICO Score 8 version. Different sampling parameters may generate different findings compared with other similar analysis. Analyzed credit data did not contain personal identification information. Metro areas group counties and cities into specific geographic areas for population censuses and compilations of related statistical data.

This story originally appeared on Experian and has been independently reviewed to meet journalistic standards.