11 ways to secure startup funding for your business

Canva

11 ways to secure startup funding for your business

business woman on the phone with business books on desk in background

For business owners and entrepreneurs with a large amount of savings, the main obstacle to starting a business is often coming up with a viable idea. Yet many aspiring entrepreneurs have a different problem—the idea is there, but the capital isn’t.

Startup funding or startup capital is something that every new business needs to get off the ground. As an entrepreneur, however, the challenge is figuring out where to find the startup funding you need to launch your new business. On a positive note, there are many startup funding options available if you know where to look.

How do startups receive funding?

Accessing startup financing can be a struggle. Traditional banks rarely offer business loans to brand-new entrepreneurs. Before lending any funds, many lenders prefer to see a proven financial track record that demonstrates an ability to repay the funds a business loan applicant is seeking. Without that financial history, the lender does not have the foresight to predict whether your venture may be successful enough to make good on your obligation.

These challenges create quite a conundrum for would-be entrepreneurs. How do you get the capital you need to get your startup off the ground when banks are unlikely to approve you for traditional business loans?

The good news is that there are multiple ways small business owners can find the startup funding they need. Some entrepreneurs find alternative financing options to fund their startups, some turn to investors, and others rely on self-funding to get the job done. Additionally, there are a few out-of-the-box ways to access startup capital available. One of the key ways to succeed as a new business is to find the right combination of startup funding that works for you.

Startup Funding Stats

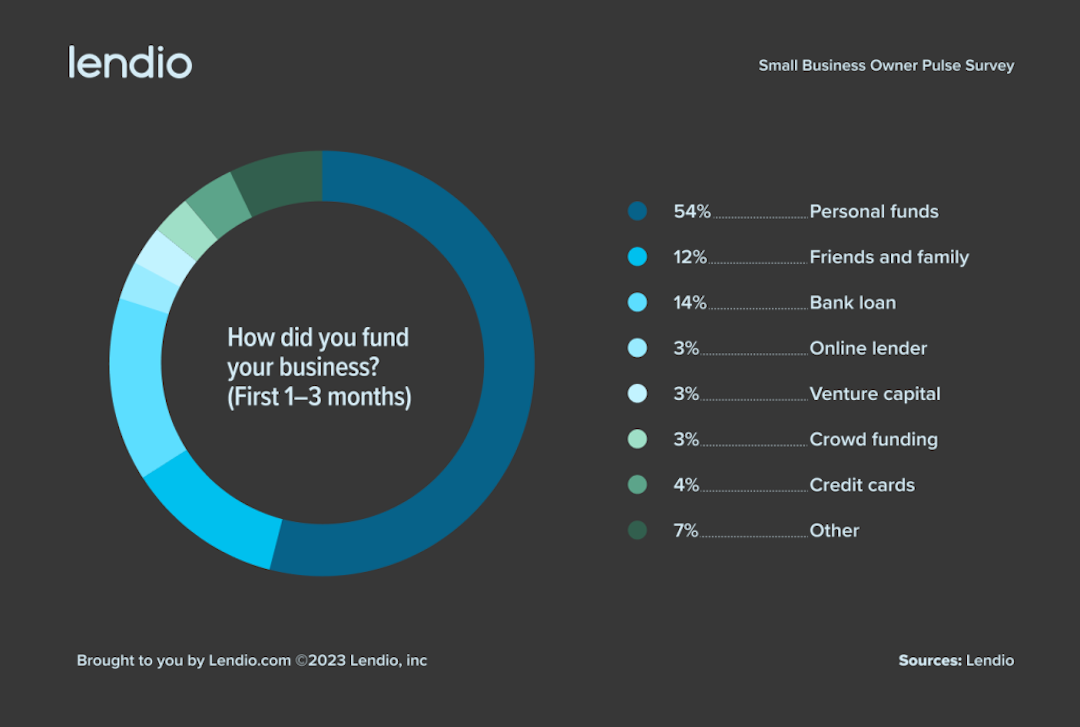

- 54% of small to medium-sized business (SMB) owners started their business with personal funds with another 12% relying on friends and family.

- 79% of SMB owners needed less than $100,000 to start their business with 43% needing less than $10,000.

- The average loan amount for a small business owner is $47,000.*

- A small business has a median of five employees when it is first funded by an outside lender.*

- A small business has been in business for about three years (a median of 40 months) when it is first funded by an outside lender.*

- *Based on internal Lendio data of 300,000+ loans funded since 2013.

![]()

Lendio

Types of startup funding

Lendio survey, “how did you fund your business? (first 1-3 months)”

Below are 11 types of business funding that are available to startups. Read on to discover whether one or several of the following startup funding options might be a good fit for your new business.

1. Alternative business loans

Small business loans from alternative lenders can be a solid funding resource for new startups. These loans often feature more lenient qualification standards compared with traditional business loans. As a result, alternative business loans may be a better fit for new businesses that are unable to qualify for other types of business financing.

In addition to less stringent requirements, alternative business loans also feature other benefits such as credit-building potential and faster funding speed. And these small business loans may offer more flexibility when it comes to how you use the money you borrow as well.

2. SBA startup loan

The Small Business Administration (SBA) is typically known for providing loans to established businesses. However, that doesn’t mean there’s no hope for an entrepreneur who’s trying to get their new business venture off the ground.

If you are able to meet the SBA’s borrowing requirements, you may be able to qualify for an SBA loan even as a startup. Generally, these loans are available to partially financed startups. The SBA likes to see the business owner have some “skin in the game” with around 30% of the owner’s own money in the business. The SBA also prefers to work with startups where the owner has some experience in the industry and in management.

It’s also important to note that the SBA itself does not issue loans. Rather, the agency establishes the guidelines for an approved intermediary and guarantees a percentage of the loan (in the case of default) which minimizes the risk to the lending partners. This financing vehicle is available to small businesses when funding is otherwise unavailable on reasonable terms. To learn more about SBA loans for startups, or to see if your business qualifies, check out this helpful SBA loan guide.

3. Microlenders

Entrepreneurs who cannot secure startup funding from other sources may also want to consider working with microlenders. Microlenders are often non-profit organizations that offer loans to small business owners—sometimes including startups—for small amounts. The loan amounts from microlenders can vary, but frequently range from $5,000 to $50,000.

Some microloans are available to specific categories of small business owners, such as women-owned businesses or minority-owned businesses. But other microloans may be obtainable by entrepreneurs that fit in broader categories.

The Small Business Administration also offers a microloan through SBA funding intermediaries for up to $50,000. The SBA microloan option does not require any collateral from the borrower and is available to eligible businesses, including startups.

4. Business line of credit

Business lines of credit are among the most flexible ways to help fund your startup. These credit lines can provide a business owner with quick capital, which they can use to meet a variety of business needs or resolve a cash flow gap.

When you open a business line of credit, the lender gives you a credit limit which represents the maximum amount you can borrow on the account. You are not required to use any of the funds until you need them, and the lender only charges interest when you access your credit line.

As you repay the money you borrowed, you also eliminate the interest the lender charges you. At the same time, you regain the ability to borrow against the same credit line again in the future—up to the credit limit—as long as the account remains open and in good standing (and the draw period is active on your account).

5. Business credit card

A business credit card could be another helpful type of startup funding to consider when you open a new business. Even if your business is brand new, you might qualify for this type of account if you have a good personal credit score.

There are many ways that a business credit card may benefit your new startup. First, a well-managed business credit card might help you build good business credit for the future, if the card issuer reports the account to one or more of the business credit reporting agencies. And a business credit card can also be valuable for helping you keep personal and business expenses separate.

You can also use a business credit card to help you manage business cash flow. However, it’s best to pay off your full statement balance each month if possible to avoid paying expensive interest charges on the account.

Finally, some business credit cards feature valuable rewards or cash back benefits. And while you should never spend extra money to chase rewards, there’s nothing wrong with earning extra perks on purchases that you already need to make for your business anyway.

6. Crowdfunding

Crowdfunding is another strategy that some entrepreneurs use to generate funding for new startups. Websites like Kickstarter and Indiegogo are examples of helpful tools that can help entrepreneurs raise small amounts of money from a large number of investors.

In addition to equity crowdfunding (as described above), some small business owners use debt crowdfunding to borrow small amounts of money from numerous lenders. Donor crowdfunding is another option to consider as it allows entrepreneurs to raise donations to support their business goals.

When the crowdfunding process is successful, it can result in an influx of startup funding to support a small business’ goals. However, results can vary and many entrepreneurs find that crowdfunding campaigns fall short of reaching their funding needs.

7. Venture capital

You may be able to get funding from investors for your startup in the form of venture capital investments. With venture capital, you give up partial ownership in your business in exchange for investments.

Venture capitalists take on a lot of risk. There’s a chance these investors could lose all of their money if a new business venture doesn’t succeed. As a result, most venture capitalists typically focus on working with companies that display high-growth potential.

As mentioned, you typically need to be prepared to offer partial ownership in your company in exchange for venture capital investments. You might also have to agree to allow investors to play an active management role as well, or at least have a seat on the board of directors. By taking a more active role in the startups in which they invest, venture capitalists often aim to improve their chances of success.

8. Startup accelerators

A startup accelerator is a small business mentoring program that has the goal of accelerating the growth of your new business venture. Typically, you must apply to be accepted into a startup accelerator, and you’ll need more than a good business idea to qualify. Many startup accelerators require startups to have an actual product (or at least a prototype) ready to produce and promote.

If a startup accelerator program approves your application, it will typically require you to sign over a percentage of equity in your company (often 5% to 10%) to secure a spot in the training program. Should the accelerator help you find other investors, you may have to surrender additional equity to secure more startup capital in the future.

9. Small business grants

Small business grants represent another unique and appealing way for startups to seek funding. Unlike business loans and other types of financing, you do not have to repay grants, nor does this type of funding feature the added expense of interest or fees.

On the other hand, competition tends to be high for small business grants. Therefore, you should be prepared to conduct research and often submit numerous grant applications if you hope to use this strategy to fund your new business venture.

Even if you apply for dozens of grants, there’s no guarantee that you’ll receive the funding you seek. But it doesn’t hurt to try as long as the process doesn’t become so time-consuming that it keeps you from completing other important tasks in your startup business journey.

10. Personal savings and credit

Many small business owners rely on personal savings or personal credit to fund their startup business ventures. A Lendio survey found that 54% of startups receive capital from personal savings. Data from the Federal Reserve also shows that 46% of small businesses use personal credit cards.

It’s important to understand that using personal funds or credit to invest in your own startup carries significant risks. For example, some entrepreneurs might withdraw funds from savings or retirement accounts to launch a new business venture. Yet before you consider taking such a big risk, it’s important to consider what would happen if the new business failed and make sure that possibility is something you could survive.

11. Family and friends

Some small business owners have the privilege of being able to turn to family and friends for support of their new business ventures. And whether your loved one wants to get involved as an investor, a lender, or a donor, receiving a helping hand from someone close to you can mean the world when you’re working hard to turn your business dreams into reality.

According to a Lendio survey, around 12% of small business owners used funds from friends or family. Yet before you accept loans, investments, or donations from loved ones, it’s important to consider the potential hidden cost.

Even the best-made business plans do not always succeed. If your startup fails and you’re unable to repay your loved one (or if their investment turns into a bad one), that loan or investment could become a financial loss for your friend or family member and damage important relationships. So, before you accept any startup funding from loved ones, it’s important to put all of the loan or investment terms in writing and have an honest conversation about the risks involved.

Next steps

There are many different ways to get startup capital for your business without a traditional bank loan. So take the time to review your options and figure out which ones work the best for you. If you decide to borrow money for your startup, it’s also wise to compare multiple financing options to make sure you find the best deals available for your situation.

As a responsible business owner, it’s also important to understand how much financial assistance you need and can afford to repay. Before you apply for any financing you should have a plan in place to pay back the money you borrow without putting yourself or your new business under financial strain.

This story was produced by Lendio and reviewed and distributed by Stacker Media.